Top 10 Auto Insurance Myths Debunked (2025): Facts Every Alabama Driver Should Know

Originally published: July 2024 | Updated: October 2025

Auto insurance is critical to responsible car ownership, but many people fall prey to common myths.

These misconceptions can lead to a better understanding of coverage, costs, and claims.

Understanding the facts behind these myths will help you make informed decisions about your auto insurance.

This article aims to debunk some of the most prevalent car insurance myths, providing drivers with clarity and peace of mind.

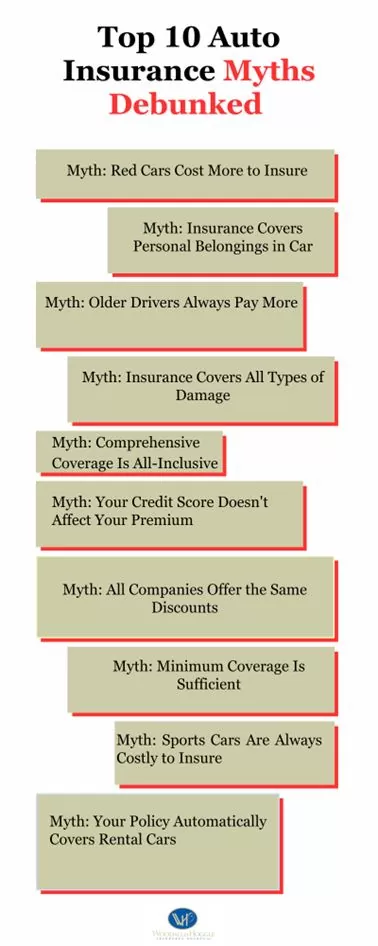

1) ‘Red cars are more expensive to insure’

Car color does not affect your auto insurance premium. Insurers base rates on vehicle make, model, age, location, and driver history. They do not consider paint color when setting costs.

The color of a car does not influence insurance rates. Insurers don’t even ask for this information.

2) ‘Insurance covers personal belongings in the car’

Standard car insurance typically does not cover personal belongings, such as laptops, phones, or bags. These items are typically protected under homeowners or renters insurance, unless you opt for additional coverage.

Some insurance policies may offer optional add-ons for personal belongings, but this is not a standard feature. Homeowner’s or renter’s insurance might protect those needing coverage for their belongings.

Always check your specific policy details to understand what is covered.

Woodall & Hoggle Insurance Agency helps Alabama drivers find auto insurance that fits their lifestyle and budget. Compare policies designed for real savings—get started today by contacting us.

If you’re ready to get

started, call us now!

3) ‘Older Drivers Always Pay More’

Older drivers don’t always pay higher premiums. Many benefit from lower rates due to their experience and safe driving records, although very elderly drivers may see increases. Shopping around helps.

While younger drivers typically have higher premiums due to inexperience, older drivers can benefit from discounts. They often have more years of driving experience and fewer accidents.

However, in some cases, very elderly drivers might see their rates increase. This can happen if insurers believe their reflexes and vision may have declined. Older drivers need to shop around for the best rates.

4) ‘Your insurance will cover all types of damage.’

Auto insurance does not cover every kind of damage. Standard policies typically exclude wear and tear, mechanical breakdowns, and floods, unless you add comprehensive or special coverage to your policy.

For instance, damage from natural disasters like floods might only be covered if you have comprehensive insurance.

Mechanical breakdowns or wear and tear are typically not covered under standard policies.

It’s important to read the details of your policy. Consider additional coverage if you want protection against a wider range of risks.

Check with your insurance provider to understand what is and isn’t covered.

5) ‘Comprehensive coverage means everything is covered.’

Comprehensive insurance only covers non-collision events, such as theft, fire, vandalism, or animal strikes. It does not cover collision damage or regular wear and tear, so additional coverage may be necessary.

Comprehensive coverage is specifically designed to handle non-collision incidents. It typically covers events like fire, theft, and natural disasters. For example, if your car is stolen or damaged by falling tree branches.

However, comprehensive coverage does not cover everything. It won’t pay for damages from a car accident caused by a collision. For that, you need collision insurance.

Animal-related accidents, such as hitting a deer, are typically covered under comprehensive insurance. However, regular wear and tear, mechanical breakdowns, and collision damage are not included.

For complete protection, consider additional types of coverage, including collision and liability insurance.

Bundle home and auto coverage with Woodall & Hoggle Insurance Agency for affordable protection across North Alabama. Save more while protecting what matters most—schedule your policy review now.

If you’re ready to get

started, call us now!

6) ‘Your credit score doesn’t affect your premium.’

Credit scores do affect premiums in Alabama. Drivers with poor credit can pay up to 80% more than those with good credit. Improving credit lowers insurance costs.

Having a poor credit score can significantly increase the cost of your car insurance. Drivers with bad credit scores may pay 80% more for their premiums than those with good credit.

Even drivers with average credit scores pay higher rates than those with excellent credit. For example, drivers with a very good credit score may pay around $1,591, while those with fair credit pay approximately $2,272.

This means improving your credit score can help lower your insurance costs.

7) ‘All insurance companies offer the same discounts.’

Insurance discounts vary by company. While most offer bundling and safe-driver savings, some provide unique discounts for telematics, new cars, or safety features. Always compare providers.

Some insurers offer discounts for bundling policies, such as home and auto. Others may offer savings for participating in safe driving programs or for owning certain safety features in your car.

It’s important to compare offers. Different companies may offer unique promotions or special deals that others do not. For example, some might offer discounts on new cars, as mentioned here.

Shopping around and looking at quotes from multiple providers can reveal these differences. This way, drivers can find the best deals that suit their needs and situations.

8) ‘Minimum coverage is sufficient’

Alabama’s 25/50/25 minimum liability coverage meets state law but often leaves drivers exposed. Serious accidents can exceed limits, making higher liability, collision, and comprehensive coverage safer.

While minimum coverage meets state laws, it often falls short when covering actual costs. Minimum coverage might be insufficient if an accident results in significant damage or medical expenses.

In such cases, the driver may need to pay the remaining costs out of pocket, resulting in financial strain.

Most experts recommend considering higher coverage limits. Comprehensive and collision coverage provides better protection for various scenarios.

Drivers should assess their own needs and risks. Understanding the implications of minimum coverage can help make informed insurance decisions.

9) ‘Sports cars are always more costly to insure’

Sports cars are not always the most expensive to insure. Rates depend on safety features, crash test ratings, and the driver’s profile. Careful drivers may pay less even with sports models.

Safety features, driving history, and the car model play crucial roles. Some sports cars have high safety ratings, resulting in lower insurance costs.

Shopping around can also help. Comparing quotes from different insurance companies can reveal affordable options.

Lastly, the driver’s profile significantly impacts rates. Age, driving experience, and history affect premiums. Even a sports car can have manageable insurance costs for a careful driver.

10) “Your policy will cover rental cars automatically.”

Not all auto policies extend to rental cars. Coverage depends on your insurer and policy. Rental companies may offer damage waivers, but you should confirm before driving.

Some policies extend coverage, but only under certain circumstances.

It’s crucial to confirm coverage specifics with your insurer. They can clarify terms and limits. Sometimes, separate rental car insurance is needed for complete protection.

Rental companies often offer collision damage waivers. This waiver covers damages or theft, but as Forbes mentioned, it usually comes at an extra daily cost.

Drive with Assurance: Choose Woodall & Hoggle for Your Auto Insurance

At Woodall & Hoggle, we understand the roads you travel. Our tailored auto insurance plans in Guntersville, Alabama, are designed to offer you the security and peace of mind you deserve.

With additional comprehensive home, business, and life insurance services, we protect every aspect of your world. Our local expertise means we’re not just an agency but your neighbors.

From new drivers to long-time residents, Woodall & Hoggle Insurance Agency offers auto insurance tailored to Huntsville families. Drive with peace of mind every day—contact us today.

Contact Us Today For An Appointment

Frequently Asked Questions

Can the color of my car affect my insurance premium?

No. Car color does not impact auto insurance rates in Alabama or anywhere else. Insurers base premiums on your vehicle’s make, model, safety features, age, and your driving record—not the paint color.

Is it true that new drivers always pay more for car insurance?

Yes. New drivers in Alabama typically pay higher premiums because they are considered high-risk. This applies to both teenagers and adults with no driving history. Over time, building a safe driving record usually lowers costs.

Will my car insurance rates decrease when I turn a certain age?

Often. Rates tend to drop around age 25 as drivers gain more experience and lower risk profiles. However, this isn’t guaranteed—factors like accidents, tickets, credit score, and the type of vehicle still influence premiums in Huntsville.

Do parking tickets have an impact on my car insurance rates?

Generally, no. Parking tickets do not usually affect insurance premiums in Alabama. Insurers focus on moving violations, crashes, or DUIs. Still, unpaid tickets could lead to license issues, which indirectly affect your coverage or costs.

Does purchasing a sports car automatically increase my insurance cost?

Not always. Sports cars often have higher premiums, but rates also depend on safety ratings, repair costs, and your driving record. A cautious Huntsville driver with good credit and a clean record can sometimes secure competitive rates even on performance vehicles.

Are older cars cheaper to insure than newer models?

Not necessarily. While older cars may be less expensive to repair, they often lack the advanced safety technology found in newer models. Newer models with crash-avoidance systems or higher safety ratings may actually be cheaper to insure despite their higher sticker price.

What are the minimum auto insurance requirements in Alabama for 2025?

Alabama requires minimum liability coverage of 25/50/25: $25,000 for bodily injury per person, $50,000 per accident, and $25,000 for property damage. These limits comply with state law but are often insufficient to cover major accidents in Huntsville.

Does my credit score affect car insurance rates in Alabama?

Yes. Alabama insurers use credit-based insurance scores. Drivers with poor credit can pay up to 80% more for premiums compared to those with excellent credit. Improving credit can help Huntsville drivers save on coverage.

How much does car insurance cost in Huntsville, Alabama?

In 2025, Huntsville drivers pay around $146 per month for full coverage, on average. Teen drivers may pay over $500 monthly, while drivers requiring SR-22 filings average about $190. Rates vary by ZIP code, driving record, and insurer.