Multi-State Business Insurance: Complete Coverage Guide for Expanding Companies

Date Posted:

July 28, 20254:41 am

Growing a business across state lines opens up a world of possibilities. But it also throws a whole new set of insurance hurdles at you—ones that can trip up even the most seasoned owners.

Each state brings its own insurance rules, coverage standards, and regulatory quirks. You’ve got to navigate all that if you want to keep your expanding operations protected.

Multi-state business insurance requires a coordinated approach that balances state regulations while maintaining consistent protection across all your operations.

Managing insurance for multi-state operations isn’t just about changing addresses on your policies.

Companies must assess their risk, determine what each state requires, and manage the details of actually operating in different locations.

The National Federation of Independent Business (NFIB) 2024 Multi-State Operations

A study found that 78% of businesses expanding operations across state lines experienced insurance compliance challenges¹.

The U.S. Chamber of Commerce’s 2024 Small Business Survey indicated that 23% of growing businesses experienced coverage gaps during interstate expansion².

Key Takeaways

Every state enforces different insurance requirements, which can complicate multi-state business operations.

Master, state-specific, and hybrid policies are all valid strategies depending on your expansion model.

Coverage gaps and compliance failures are common; professional support helps avoid costly mistakes.

Woodall & Hoggle’s multi-state licensing and regional expertise make them ideal for growing companies needing consistent, compliant coverage.

Understanding Multi-State Insurance Complexity

Every state enforces its own insurance laws and licensing hoops, which can be a real headache for businesses trying to grow.

On top of that, federal rules for interstate commerce layer on more requirements, so you’ve got to keep an eye on both.

State-by-State Regulatory Variations

State

Minimum Benefits

Monopolistic vs Competitive

Key Differences

Alabama

$969/week max

Competitive market

5+ employee threshold

Florida

$971/week max

Competitive market

Construction = immediate coverage

Tennessee

$1,157/week max

Competitive market

Agricultural exemptions vary

Georgia

$725/week max

Competitive market

3+ employee threshold

Texas

$963/week max

Competitive + non-subscription

Optional for most employers

Each state has its unique insurance laws that businesses must follow when operating in multiple locations. These differences add to the compliance work for companies looking to expand.

Workers’ compensation rules can be all over the map. Some states require you to buy it from state-run funds, while others allow you to use private carriers. California requires that every employee be covered. Texas? It’s optional for most businesses.

General liability minimums also vary from one location to another. New York demands higher limits than many southern states. Some places require additional coverage that others do not.

Insurance filing rules add more layers. Companies have to file different forms and paperwork with each state’s department. Businesses operating in multiple states often face challenges in staying current with all applicable laws and regulations.

Premiums jump around a lot, too. One state might charge 40% more than another for the same coverage, depending on risk and regulations.

Professional Licensing Insurance Requirements

Insurance requirements for professional licenses shift from state to state and industry to industry. If you’re licensed, you’ve got to keep up with each state’s minimums wherever you work.

Medical professionals face various demands for malpractice insurance. Florida, for example, sets higher minimums than most. Some states also insist on tail coverage when you change insurers.

Legal professionals require different levels of liability coverage, depending on where and what they practice. Real estate attorneys often need additional protection in high-volume states.

Construction contractors must meet bonding and insurance requirements that vary depending on the project size and location. Many states won’t hand over permits or licenses until you show proof of coverage.

Financial advisors and insurance agents are required to maintain errors and omissions insurance that complies with each state’s regulations. The coverage amounts and terms can vary a lot from place to place.

State boards don’t mess around—they’ll audit for insurance compliance regularly. If you drop below the required coverage in any state, you risk losing your license there.

Interstate Commerce Federal Requirements

Federal rules apply to businesses that move goods or offer services across state lines. These often trump state-specific insurance laws for interstate work.

Transportation companies must meet the Federal Motor Carrier Safety Administration’s insurance standards. Depending on what you haul and your trucks’ weight, you might need $750,000 to $5 million in liability coverage.

Aviation businesses follow Federal Aviation Administration mandates. Pilots and operators must meet federal minimums, regardless of any additional requirements imposed by individual states.

Shipping and logistics outfits keep cargo insurance that covers goods moving between states. Federal rules establish those minimums, depending on the type of freight.

Telecommunications providers serving multiple states must meet Federal Communications Commission insurance standards, which often exceed the requirements of individual states.

Companies working in interstate commerce file proof of insurance with the right federal agencies. If they drop required coverage, they can lose their operating licenses and face heavy penalties.

Expanding across state lines? Woodall & Hoggle Insurance Agency provides tailored general liability plans for multi-state operations. Contact us today to start your coverage coordination.

If you’re ready to get

started, call us now!

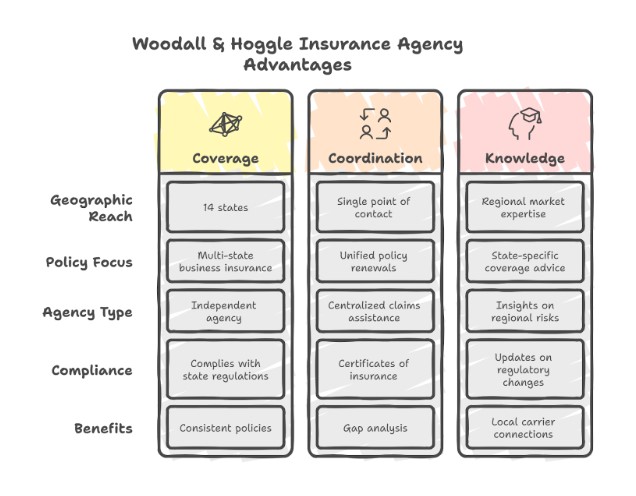

Woodall & Hoggle’s 14-State Coverage Advantage

Woodall & Hoggle Insurance Agency offers multi-state business insurance across 14 states, and they have a deep understanding of the local markets.

Their independent agency setup allows them to coordinate coverage while staying informed about regional details.

Licensed States and Specializations

Woodall & Hoggle Insurance Agency runs as an independent agency, licensed in 14 southeastern and nearby states. That reach means businesses can have consistent policies, regardless of where they operate.

They focus on a handful of key areas for multi-state clients:

Commercial general liability that works across state lines

Workers’ compensation that matches each state’s requirements

Property insurance for multiple facilities

Commercial auto coverage for fleets

As an independent agency, they work with multiple insurance carriers, not just one. That provides businesses with more options for coverage that aligns with state-specific regulations.

Their licensing setup enables them to write policies that comply with all the various state regulations. Businesses don’t have to juggle a bunch of agents in different places.

Unified Coverage Coordination

Because they’re licensed in so many states, Woodall & Hoggle make it easier for growing businesses to manage their insurance. You get one point of contact instead of chasing down different agents all over the map.

Woodall & Hoggle’s independent status allows them to shop around for coverage and prices from multiple carriers. That’s a big deal when your insurance needs shift from state to state.

They handle:

Policy renewals for every state you’re in

Claims help no matter where something happens

Certificates of insurance for any state that needs them

Gap analysis to spot differences between state requirements

This unified approach significantly reduces paperwork and headaches. It also helps keep your coverage standards steady everywhere you do business.

Local Market Knowledge

Woodall & Hoggle’s team brings extensive experience in regional insurance markets. Their crew has over 150 years of combined experience in the industry, so they are well-versed in the ins and outs of state-specific requirements.

Every state throws its curveballs for business insurance. Their local knowledge helps businesses navigate workers’ compensation rules, liability limits, and compliance standards that vary from state to state.

They offer:

State-specific coverage advice and minimum limits

Regional risk insights that affect your premiums

Local carrier connections for better pricing

Updates on regulatory changes that might impact your needs

This kind of local expertise is a lifesaver for businesses entering new states. They can spot potential gaps before they become real problems.

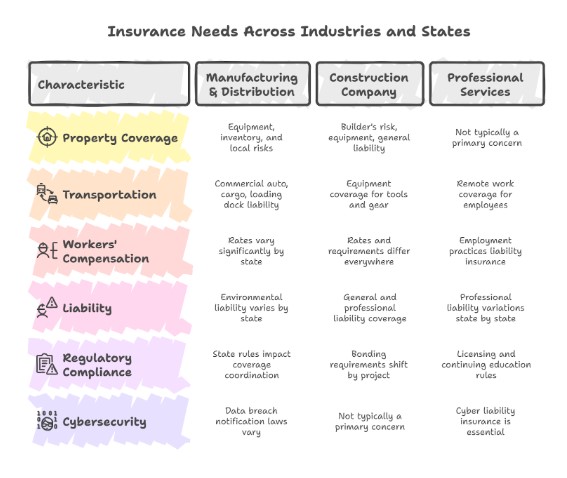

Common Multi-State Business Scenarios (Real-World Applications)

Businesses that expand across state lines encounter various insurance challenges, and the solutions depend on the specific industry in which they operate.

Manufacturers require coverage for moving equipment, construction firms must comply with project-specific regulations, and professional services must navigate liability requirements that are constantly evolving.

Manufacturing and Distribution Expansion

Manufacturers face a complex array of insurance needs as they expand into new states. Every facility needs its coverage for gear, inventory, and local risks.

Property Coverage Considerations:

Equipment breakdown insurance for machines in different spots

Business interruption coverage for supply chain hiccups

Inventory protection for goods moving between states

Distribution centers need warehouse-specific coverage. Workers’ comp rates can swing wildly from state to state, which impacts your bottom line.

Transportation Requirements:

Commercial auto insurance for delivery trucks

Cargo insurance for stuff in transit

Loading dock liability coverage

State rules can throw you for a loop. California’s environmental liability laws are stricter than most. Texas and Florida don’t see eye to eye on workers’ comp minimums.

Manufacturers have to coordinate coverage everywhere. One incident can ripple through the whole supply chain.

Construction Company Multi-State Projects

Construction companies operating in different states require insurance tailored to each project. Every state has its own bonding and liability rules for construction work.

Project-Specific Coverage:

General liability for each job site

Builder’s risk insurance for materials and work underway

Equipment coverage for tools and gear moving between states

Bonding requirements shift depending on the state and project type. Government jobs usually require larger bonds than private jobs.

Workers’ Compensation Challenges:

Rates and requirements differ everywhere

Coverage for teams moving between sites

Staying compliant with local safety rules

Professional liability insurance safeguards against design errors and construction defects. Some states give you more or less time to file claims than others.

Checking subcontractor insurance gets tricky across state lines. Each place might want different minimums from your subs.

Professional Services Expansion

Professional service firms expanding into new areas must comply with varying licensing and insurance requirements in each state.

Law, accounting, and consulting outfits all face different liability standards depending on where they work.

Professional Liability Variations:

Malpractice insurance rules change state by state

Coverage limits might need tweaking for local courts

Tail coverage if you close an office

Remote work only complicates things. Employees working from home in other states may require extra coverage.

Regulatory Compliance:

Licensing requirements affect insurance in each state

Continuing education rules vary

Different ethics standards and complaint processes

Cyber liability insurance is essential for firms that handle client data across multiple states. Data breach notification laws vary from one jurisdiction to another.

Employment practices liability insurance must keep pace with state employment laws. California, for example, has tougher overtime rules than most, which can raise your risk for claims.

Professional service firms need the right insurance for multi-state operations to protect against all these shifting risks.

Companies growing into new states need a plan to handle insurance efficiently. There are several primary ways to coordinate coverage, each with its trade-offs in terms of control, cost, and complexity.

Master Policy Approach

A master policy centralizes coverage under one comprehensive plan that covers multiple states. This setup streamlines administration, providing a single point of contact for claims, renewals, and policy management.

Key advantages include:

Streamlined billing and payment processes

Consistent coverage terms across all locations

Less administrative hassle for your internal teams

Stronger negotiating power with insurance carriers

Companies with similar operations in every state typically derive the most benefit from a master policy. Workers’ compensation for multi-state businesses often works better with this consolidated approach.

Implementation requirements:

Check that your carrier is licensed in all operating states

Make sure coverage meets each state’s minimum requirements

Set up clear communication between all locations

Centralized claims reporting procedures

Companies need to review state-specific requirements closely. Some states may require additional endorsements or coverage adjustments to remain compliant.

State-Specific Policy Approach

This method involves purchasing separate insurance policies for each state where you conduct business. Each policy gets tailored to fit that state’s rules and business climate.

Benefits of state-specific policies:

Full compliance with local insurance laws

Coverage customized for regional risks

Possible cost savings in lower-risk states

Closer relationships with local insurance providers

This approach is particularly effective for companies with operations in multiple states. Essential insurance coverage for multi-state business operations often requires this more targeted approach.

Administrative considerations:

Multiple renewal dates to juggle

Separate claims processes for every state

More paperwork and documentation

Need for local insurance know-how

You’ll need to keep detailed records for each policy. That means tracking coverage limits, deductibles, and your carrier’s contact info for easy management.

Hybrid Solutions (Best of Both Worlds)

Hybrid approaches mix master and state-specific policies. Some companies maintain a master policy for core coverage and add state-specific endorsements to comply with local regulations.

Common hybrid structures:

Master liability policy with state-specific workers’ comp

Centralized property coverage, local auto policies

Umbrella policy over several state policies

Regional groupings of similar states under shared policies

This flexibility lets companies balance cost and compliance. Multi-state insurance coverage strategies often suggest hybrid solutions for complex operations.

Implementation steps:

Assess risks and requirements by state

Decide which coverage types you can centralize

Pinpoint policies that need local customization

Set up coordination protocols between carriers

Create unified reporting and claims procedures

Companies should regularly revisit their hybrid approach. If your business grows or state regulations change, you’ll need to adjust your coverage.

From workers’ comp to commercial auto, Woodall & Hoggle simplifies multi-state insurance with flexible, compliant coverage options. Schedule a policy review now to keep your expansion on track.

If you’re ready to get

started, call us now!

Cost Management for Multi-State Operations

Smart cost management enables businesses to save money while maintaining comprehensive coverage across state lines.

You can cut expenses by planning premiums strategically, streamlining admin work, and building a solid risk management program.

Premium Optimization Strategies

Bundling policies across several states can lower your insurance costs. Multi-state coverage providers sometimes offer discounts if you buy workers’ comp, general liability, and other policies together.

Key Premium Reduction Methods:

Bundle multiple coverage types with one insurer

Negotiate for multi-state volume discounts

Pick higher deductibles for lower premiums

Use safety programs to qualify for discounts

Compare rates between regional and national insurers. Sometimes, regional carriers offer lower prices than national ones in specific states, although national insurers provide consistency.

Review your policies annually to identify new opportunities for savings. As your business evolves or grows, your insurance needs will change accordingly.

Administrative Cost Reduction

Combining billing across states can shrink paperwork and lighten your admin load. A single billing system means fewer vendors and payment headaches.

Administrative Efficiency Tools:

Unified policy management systems

Centralized claims reporting

Digital document storage

Automated compliance tracking

Insurers who handle multi-state compliance save you time and effort. You won’t need separate legal or admin teams in every state that way.

Switching to electronic filing reduces costs associated with paper documentation. Digital records also make audits and renewals faster and less painful.

Risk Management Program Benefits

Strong risk management programs can lower your premiums in every state. Insurance providers for multi-state businesses often offer real discounts to companies with a good safety record.

Cost-Saving Risk Management Elements:

Employee safety training programs

Regular workplace inspections

Incident reporting systems

Return-to-work programs

Fewer claims mean lower premiums. Maintaining consistent safety standards everywhere reduces the risk of major accidents or lawsuits.

Good risk management also cuts indirect costs. Fewer injuries mean less downtime and fewer expenses for replacement workers.

Investing in safety equipment and training usually pays off—most companies see reduced insurance costs within two years.

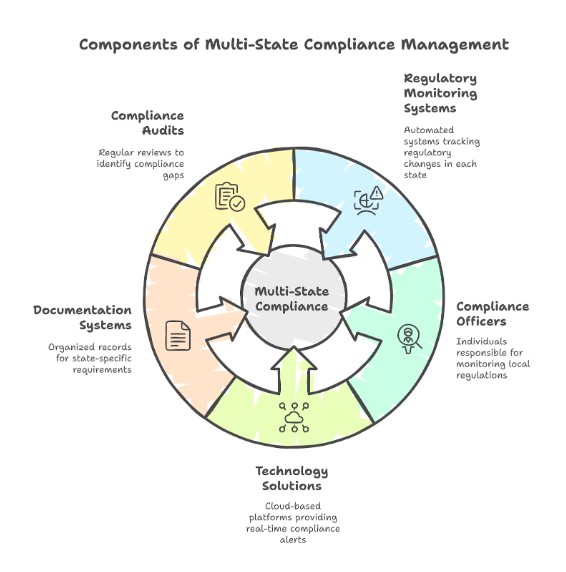

Compliance Management Across States

Companies operating in multiple states require a system for tracking evolving regulations and maintaining accurate documentation.

Multi-state compliance challenges require dedicated monitoring and organized record-keeping to avoid penalties.

Regulatory Monitoring Systems

Businesses should establish automated systems to monitor regulatory changes in every state where they operate. Every state brings its own rules for insurance, licensing, and employment laws.

Key monitoring components include:

Daily regulatory update alerts for each state

Automated compliance deadline notifications

State-specific requirement tracking databases

Legal change impact assessments

Appoint compliance officers for each region. They’ll keep an eye on local regulations and coordinate with headquarters when updates are needed.

Tech can help here. Cloud-based compliance platforms send real-time alerts when rules change and track filing deadlines for you.

Multi-state employers often face challenges when workers cross state lines. Remote work policies must reflect the varying state employment laws and insurance requirements applicable to each location.

Regular compliance audits highlight any gaps. Try doing quarterly reviews of all state requirements and your current coverage.

Documentation and Record Keeping

Effective documentation systems help you avoid trouble and facilitate the processing of insurance claims. You’ll need to maintain separate records to comply with each state’s requirements.

Essential documentation includes:

State-specific insurance certificates

Employee work location records

Compliance training documentation

Regulatory correspondence files

Digital record management is most effective for multi-state setups. Cloud storage enables authorized individuals to access what they need from anywhere, while maintaining security.

Set retention schedules for each document type. Every state has its own rules for how long you need to keep records.

Multi-state compliance checklists help you stay on top of documentation. Update these checklists when regulations shift.

Backups are a must. Keep both digital and physical copies of your most important compliance documents, just in case.

Monthly documentation audits help you catch missing records before they cause problems.

Implementation Planning for Multi-State Expansion

Companies need a clear plan to check their readiness and map out next steps before expanding insurance coverage across state lines.

This involves conducting a thorough risk assessment and implementing strategic planning to ensure compliance with all applicable state regulations.

Pre-Expansion Assessment

Business leaders should thoroughly review their current insurance portfolio before expanding into new states. This helps identify coverage gaps and potential compliance issues.

Review existing policies to see what carries over. Workers’ compensation requirements vary significantly by state, making this step crucial for businesses operating across multiple states.

Risk managers must assess exposures in every target state. Tort laws, damage caps, and regulations can change what kind of insurance you need.

Workers’ compensation coverage can become complex due to state-specific rules and variations in rates.

Implementation Strategy

Organizations should roll out insurance coverage in phases as they expand their operations. Prioritize high-risk locations and make sure there are no coverage gaps during the switch.

Factor licensing requirements and regulatory approvals into your timeline. Some states require advance notice or special paperwork before coverage takes effect.

Set up clear communication with your insurance providers. Regular coordination meetings ensure everyone is on the same page regarding coverage requirements and timing.

Key implementation steps include:

Policy modification requests 30-60 days before expansion

Adjust premiums based on new state rates

Update certificates of insurance for new locations

Notify employees about coverage changes

Business insurance providers often suggest staggered rollouts to keep admin work manageable and verify coverage at each new site.

Getting Started with Multi-State Coverage

Companies moving into new states need a systematic approach to assess their insurance needs and establish solid coverage.

That usually means a deep risk assessment and some professional help to navigate all those state rules.

Initial Assessment Process

Business owners should start by comparing their current insurance to what multi-state operations require. This helps identify coverage gaps and indicates which policies require state-specific adjustments.

Key evaluation areas include:

Current policy territories and limitations

State-specific coverage requirements

Employee locations and work activities

Physical business locations and assets

Document all business activities by state—where employees work, where equipment sits, and where you serve customers. Each state has its insurance requirements that affect your coverage.

Workers’ compensation requirements vary a lot between states. Some want coverage for any employee working there, while others set different thresholds.

Review general liability, property, and professional liability policies. Many of these have territorial limits that might not fit your multi-state plans.

Implementation Support

When you’re setting up multi-state coverage, you need professional insurance guidance.

Qualified insurance agents or brokers can assess specific needs and recommend the most suitable coverage for each individual’s situation.

Implementation steps include:

Policy modification or replacement

State registration processes

Premium calculation adjustments

Compliance documentation setup

Insurance professionals help you figure out which states require separate policies and which just need endorsements.

If you can’t get everything from one carrier, they’ll coordinate with several insurance companies.

Some insurance providers offer consolidated billing, which means you receive a single monthly statement for all your multi-state coverage.

This makes administrative work less painful and reduces billing headaches.

It’s smart for companies to set up ongoing compliance monitoring. State rules change all the time, so you’ll want a way to keep up with updates that could impact your coverage.

Need help managing insurance in multiple states? Woodall & Hoggle Insurance Agency ensures coverage compliance in 14 states where it is licensed. Contact us now to streamline your protection strategy.

Contact Us Today For An Appointment

Frequently Asked Questions

What is multi-state business insurance?

Multi-state business insurance provides coordinated coverage across different states, ensuring compliance with each state’s specific laws and minimizing coverage gaps for expanding companies.

Why do insurance requirements vary between states?

Each state has its regulations, minimum coverage thresholds, and enforcement practices, which affect the requirements for workers’ compensation, general liability, and professional liability insurance.

What federal rules apply to multi-state businesses?

Federal laws apply to transportation, aviation, logistics, and telecom sectors, often requiring businesses to meet higher liability minimums and file proof of insurance with federal agencies.

How do I coordinate insurance across multiple states?

Businesses can use master policies, state-specific plans, or hybrid structures. Working with an agency licensed in multiple states simplifies policy management and ensures compliance with regulations across various states.

What are common coverage gaps for growing businesses?

Gaps often occur in workers’ compensation, professional liability, and auto coverage due to differences in state laws, employee classification, and inconsistent policy limits.

How can I reduce insurance costs while expanding into new states?

Bundle policies, implement risk management programs, review deductible strategies, and work with independent agents to compare rates from multi-state carriers.

Sources:

National Federation of Independent Business, “Multi-State Business Challenges 2024.” – NFIB.org, May 2024.

U.S. Chamber of Commerce, “Small Business Interstate Commerce Report 2024.” – uschamber.com, July 2024.