Alabama Business Insurance Requirements: Complete 2025 Compliance Guide

Originally published: July 2025 | Updated: August 2025

Alabama business owners face a unique set of rules and responsibilities regarding insurance coverage each year.

To remain legally compliant in 2025, companies must carry specific types of insurance based on their size, industry, and employee count, and they must also stay up-to-date with changing state regulations.

This applies to everything from general liability and workers’ compensation to more specialized requirements. Compliance becomes a top priority for any business in Alabama, regardless of its size.

Knowing which policies are legally required—and which are just smart to have—can save owners from expensive mistakes. Rules change, so keeping up with the latest Alabama business insurance requirements is just part of running a business here.

This guide outlines the coverage you need and provides access to the most up-to-date information. Hopefully, it’ll help Alabama businesses make better decisions and avoid headaches down the road.

Key Takeaways

Alabama requires workers’ compensation, commercial auto, and sometimes professional liability insurance for legal business operations.

Penalties for non-compliance can be severe, including daily fines of $1,000 and license suspensions.

Coverage varies by industry—construction, healthcare, finance, and hospitality all have unique requirements.

Working with an independent agency like Woodall & Hoggle helps reduce costs, stay compliant, and simplify multi-state coverage.

Mandatory Business Insurance In Alabama (Legal Requirements)

Alabama law stipulates that certain types of business insurance are mandatory for specific situations.

If you employ at least one person, you need to meet state coverage standards. Business vehicles and licensed professionals have their own set of rules as well.

Alabama Department of Labor enforcement data shows that penalties for workers’ compensation violations can reach $1,000 per day per uncovered employee¹, with the

The Alabama Department of Insurance reported suspensions of business licenses for insurance compliance failures in 127 cases during 2024².

Workers’ Compensation Insurance (Alabama Department of Labor)

If you run a business in Alabama with one or more full-time or part-time employees, you must have workers’ compensation insurance. This law protects employees who are injured or become ill as a result of their job.

Under Alabama Code § 25-5-50, employers with five or more employees are required to provide workers’ compensation coverage¹.

Construction industry employers must provide coverage for all employees, regardless of the number, as specified in the Alabama Department of Labor regulations².

The Alabama Department of Labor enforces these rules and checks for compliance. Employers who skip this coverage risk fines, lawsuits, or even being forced to shut down.

There are exceptions for businesses with fewer than five employees, farm laborers, and domestic workers; however, most companies don’t qualify for these.

Coverage pays for medical bills, wage replacement, and rehabilitation services for employees injured on the job.

It’s designed to reduce disputes and create a safer workplace. For more details on requirements and penalties, check out this guide to Alabama business insurance.

Commercial Auto Insurance (Alabama Department of Public Safety)

If your company owns or operates vehicles for business, you have to carry commercial auto insurance under Alabama law. The Alabama Department of Public Safety enforces this requirement.

Coverage minimums are:

$25,000 for bodily injury per person

$50,000 total per accident

$25,000 for property damage

This insurance covers delivery trucks, company cars, and even employee vans. Personal auto policies won’t suffice if the vehicle is used for business purposes. Without the right coverage, you could face huge fines, lose your vehicle registration, or get sued after an accident.

Professional Liability (Licensed Professions)

Professionals working in medicine, law, real estate, or engineering typically require professional liability insurance. You might hear it referred to as errors and omissions (E&O) insurance.

Alabama requires some licensed professionals to carry it to keep their license or get certain contracts. This insurance covers claims related to mistakes, missed deadlines, or negligence that result in financial losses for clients.

Doctors need malpractice insurance, and lawyers may need E&O coverage for some courts or firms. Policy limits and rules change depending on the profession.

Carrying this insurance helps professionals avoid expensive lawsuits and maintain an active license. It’s advisable to consult with your licensing board to determine the specific requirements for your field.

Need help understanding your 2025 insurance obligations? Woodall & Hoggle Insurance Agency offers tailored general liability coverage for Alabama businesses. Contact us to get started.

Insurance requirements in Alabama aren’t one-size-fits-all. Every industry faces different legal responsibilities and risks, so the coverage you need can look very different depending on your sector.

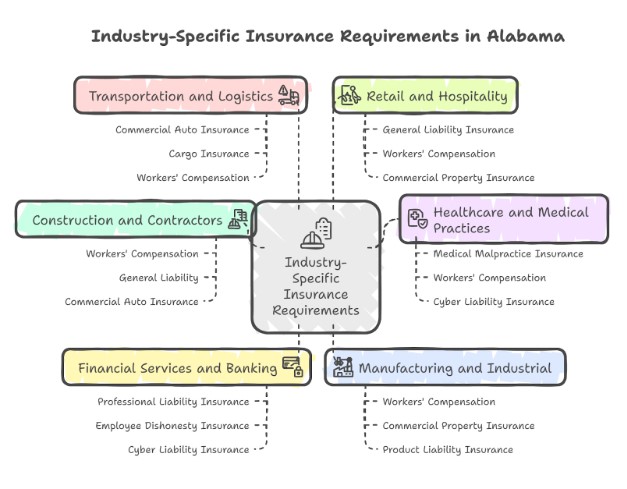

Construction And Contractors

If you’re in construction and have at least one employee, Alabama law says you must provide workers’ compensation. This covers job injuries and medical bills.

General liability is also a must, protecting you from property damage and third-party injury claims. Many contractors need commercial auto insurance for company vehicles.

Builders’ risk policies cover materials and supplies while you’re on the job site. If you handle design or project management, you may also need professional liability insurance.

Contractors on public jobs often need to obtain bonds—bid, payment, or performance bonds—to guarantee the work is completed and protect the client.

Always verify the bonding and insurance minimums for large projects with the contracting agencies to ensure compliance.

Healthcare And Medical Practices

Healthcare providers—such as clinics, doctors’ offices, and urgent care centers—require multiple types of insurance. Medical malpractice insurance is crucial for protecting healthcare providers against lawsuits arising from errors or negligence in patient care.

Cyber liability insurance is gaining popularity as data breaches and digital theft incidents increase. Some providers offer group health insurance to attract and keep good employees.

Staying HIPAA compliant is essential, and it can influence the type of insurance you choose.

Financial Services And Banking

Banks and financial service providers require insurance tailored to their specific regulatory needs and security risks.

Professional liability (also known as errors and omissions) insurance is crucial for banks, credit unions, accountants, and advisors to protect against mistakes in their work.

Alabama banks are also required to maintain insurance for employee dishonesty or fidelity bonds to cover theft or fraud committed by staff.

Cyber liability is now a standard requirement due to the increasing amount of sensitive data and the prevalence of cyberattacks.

Directors and officers liability insurance shields leadership from lawsuits over mismanagement or compliance issues.

Since financial businesses are subject to audits and reviews, maintaining accurate records and adhering to policy requirements is a crucial part of the job.

Manufacturing And Industrial

Manufacturers in Alabama face risks such as property damage, workplace injuries, equipment breakdowns, and product liability claims. You need workers’ compensation for employees, especially in high-risk industrial settings.

Commercial property and equipment breakdown insurance covers repairs or replacements in the event of accidents or disasters. Product liability insurance is smart—sometimes even required—since defective products can cause problems after sale.

Plants that store or use hazardous materials often need pollution liability insurance. Reviewing local and federal environmental rules regularly helps you stay compliant and avoid fines for accidental pollution.

Transportation And Logistics

Trucking, hauling, and delivery companies are required to meet strict coverage requirements. Commercial auto insurance is necessary if you use vehicles for business purposes.

If you cross state lines, you might need higher coverage under federal FMCSA rules. Cargo insurance protects goods in transit, covering losses in the event that shipments are lost or damaged.

Workers’ compensation is a must for drivers, loaders, and warehouse staff. Non-owned vehicle liability is beneficial if you use rentals or personal vehicles for business purposes.

Fleet operations may require additional endorsements for specific tasks, such as transporting hazardous materials or handling oversized loads.

Retail And Hospitality

Retailers, restaurants, and hotels in Alabama need to protect themselves from customer injuries and property damage. General liability insurance is the backbone of any risk plan here.

If you have employees, you are required by law to provide workers’ compensation. Commercial property insurance covers buildings, inventory, equipment, and cash registers from theft, fire, or storms.

Liquor liability insurance is required if you serve alcohol. Product liability insurance is useful for shops selling food, drinks, or manufactured goods.

Hospitality businesses sometimes carry event insurance for weddings, conferences, or other special occasions. It’s a good way to give both owners and clients a little peace of mind.

From workers’ compensation to commercial auto, Woodall & Hoggle can simplify Alabama compliance with a single, bundled business insurance review. Schedule a call to review your coverage.

If you’re ready to get

started, call us now!

Multi-State Business Operations (Woodall & Hoggle Specialty)

When Alabama businesses expand into other states, insurance requirements and compliance challenges can get complicated fast. Local laws, minimums, and risks vary in every location you operate.

Interstate Commerce Considerations

If you cross state lines, you have to deal with each state’s rules for workers’ compensation, liability, and commercial auto insurance. A policy that works in Alabama might not be enough elsewhere.

Some states set higher minimums or require extra types of insurance. Hiring employees or transporting goods into new states means taking on new legal responsibilities.

If you miss another state’s insurance laws, you might get fined or face penalties. It helps to work with agencies that are familiar with multi-state business insurance and can tailor policies to your specific needs.

Gaps in protection pose a significant risk when operating in multiple states. Reviewing risk exposures and insurance rules for each state every year helps avoid uncovered losses or contract issues.

Common Multi-State Business Scenarios

Some businesses open offices in neighboring states, send teams to work on remote projects, or deliver products throughout the Southeastern United States. Each of these scenarios changes the type of insurance you need.

For example:

Opening new offices in Georgia, Florida, or Tennessee

Mobile teams performing services in several states

Expanding delivery routes into neighboring regions

If you operate in multiple states, you have to check the rules for each one. Worker classification and insurance limits can vary between Alabama and other states, such as Mississippi.

Working with companies like Woodall & Hoggle Insurance Agency helps you stay up-to-date. They are familiar with the ins and outs of states like Arkansas, Louisiana, Texas, and others.

Coordination Strategies

Managing compliance is easier with a checklist for every state where you do business. Here are some key steps:

List all states where you have employees, vehicles, or offices

Compare insurance requirements for general liability, workers’ compensation, and property coverage

Update policies as your operations grow

Independent multi-state insurance agencies connect you with carriers licensed in many places. Woodall & Hoggle can help coordinate everything under one program, so you don’t end up with duplicate coverage or miss any rules.

Keeping your records and renewal dates synced across states helps prevent lapses in coverage or legal trouble.

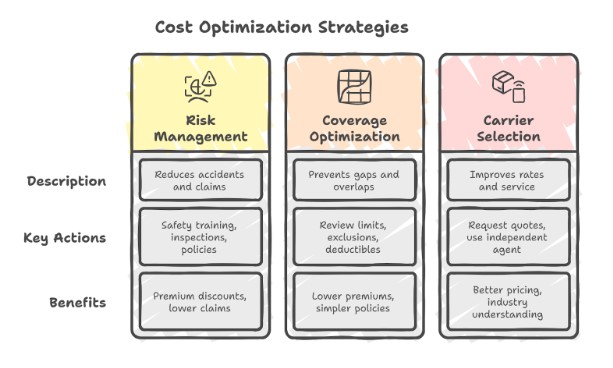

Cost Optimization Strategies For Required Coverage

Controlling business insurance costs in Alabama requires a strategic approach. You can keep expenses down—and still get the protection you need—by making smart choices in a few key areas.

Risk Management Programs

Building strong risk management programs can significantly reduce insurance costs. Safety training, clear employee policies, and regular site inspections all help lower the risk of accidents and claims.

Companies should track every incident with detailed reports. Reviewing these reports allows you to identify patterns and address safety issues before they become costly.

Some insurers offer premium discounts if you can prove your risk management is solid. Keeping a documented program—such as safety manuals, inspection checklists, and employee training logs—gives you proof to show carriers when negotiating.

Coverage Optimization

Take the time to look over your insurance policies. You want to catch gaps or overlaps and ensure you’re not paying for coverage you no longer need.

During your annual review, check liability limits, exclusions, and any optional coverages that might be outdated.

Sometimes, raising your deductible can lower your premiums, but make sure you’ve got enough cash to cover that higher deductible if something happens.

Bundling policies—like general liability, property, and business interruption—into a Business Owner’s Policy (BOP) can save you money and make things less complicated.

Carrier Selection Strategy

Shop around. Comparing insurance carriers can lead to better rates and service, no question.

Request multiple quotes every renewal cycle and check if there are any new discounts or programs for which you may qualify.

Working with an independent insurance agent can open up options from carriers that truly understand your industry.

Agents usually know which providers offer the best pricing for your specific risk profile. Building a relationship with your insurer over time can help you negotiate better terms.

Compliance Monitoring And Updates

Alabama business insurance rules are constantly evolving, particularly with the introduction of new laws in 2025.

Staying compliant means you’ve got to watch for these updates and review your insurance practices every year to make sure you’re still on track.

Regulatory Changes To Watch

For 2025, Alabama plans to tighten rules regarding digital privacy, workers’ compensation, and health coverage. You’ll probably see more detailed standards for recordkeeping and data reporting.

Insurance carriers and employers might need to submit new electronic documentation for employee coverage and claims.

The minimum required coverage is expected to increase, particularly for construction and healthcare businesses.

Companies must stay informed about updates from state agencies and regulatory bulletins. Real-time compliance tools and alerts can help track these changes, ensuring you don’t fall into a coverage gap or inadvertently violate regulations.

Annual Review Requirements

Alabama companies should review their business insurance policies annually to ensure they are in compliance. Check your license status, update your certificates of insurance, and ensure your employee classifications are accurate for workers’ compensation purposes.

Many insurers now use automated systems that send real-time alerts for missing paperwork, expirations, or regulatory updates. Businesses should keep records of all reviews and corrective actions.

Scheduled annual audits help you maintain accurate and up-to-date documentation, ensuring it is ready for any regulatory inspection. Adding compliance monitoring tools can automate much of this process.

Getting Started: Alabama Business Insurance Planning

Alabama businesses must understand the basics, including what insurance coverage is required, how to stay compliant with state regulations, and how to establish ongoing support. Knocking out these steps early can save you headaches down the road.

Initial Business Assessment

Begin by identifying the primary risks to which your business is exposed. Think property damage, legal claims, employee injuries, vehicle issues—the usual suspects.

If you run a retail shop, you may need additional coverage for theft and property damage. A construction business? Liability and workers’ comp are probably at the top of your list.

A checklist helps keep things organized:

Identify your business assets and activities

List all employees, vehicles, and equipment

Record your business location(s)

Estimate monthly revenue and payroll

When you match these risks to the right coverage, you’ll see which policies—like general liability or workers’ comp—you need to stay legal in Alabama.

Compliance Audit Process

A compliance audit checks that you’ve got the right insurance in place. Alabama law requires every company with at least one employee to have workers’ compensation coverage.

Specific vehicles and higher-risk industries may require additional coverage. Here’s a quick audit rundown:

Review current policies to find any gaps

Verify that employee classifications match your payroll

Check coverage limits against Alabama’s legal minimums

Document policy numbers and proof of insurance

If you miss something, you could face fines or even business interruptions. Many owners use state and industry checklists—such as those from the Alabama Department of Revenue—to ensure they don’t overlook anything.

Woodall & Hoggle Consultation Process

Getting professional advice can make insurance planning less stressful. Woodall & Hoggle guides clients through risk assessment, policy selection, and compliance checks.

Their process begins with a review of your company’s structure, operations, and exposures. Here’s what stands out in their consultation:

Personalized risk analysis with interviews and documentation

Policy comparison to help you find the most cost-effective choices

Annual reviews to keep you compliant and up to date

Clients report gaining insights that extend beyond the basics. Woodall & Hoggle’s agents break down confusing terms and help owners make informed decisions, staying by your side as your business evolves or changes.

Conclusion

Alabama business owners must closely monitor insurance requirements. Every year, state and industry rules may shift, which can alter your coverage needs.

You should review your business policies regularly. It’s the only way to make sure you stay in compliance.

Key areas for annual review:

General liability coverage: Most businesses need this

Workers’ compensation: Many employers must have it

Professional liability or industry-specific insurance: It depends on your field

Owners should stay informed about updates from state departments and industry groups. Otherwise, you risk running into fines or interruptions you don’t want.

Managing insurance isn’t just about buying a policy. You need to keep your records organized and stay informed about any changes that may occur.

Multi-state coverage? High-risk industry? Woodall & Hoggle Insurance Agency helps Alabama businesses stay compliant without overpaying. Contact us now to plan your 2025 insurance strategy.

Contact Us Today For An Appointment

Frequently Asked Questions

What business insurance is legally required in Alabama for 2025?

In 2025, Alabama businesses with five or more employees are required to carry workers’ compensation insurance, commercial auto insurance for business vehicles, and professional liability insurance for certain licensed professions.

Do small businesses in Alabama need workers’ compensation insurance?

Yes, if a small business has five or more employees or operates in the construction industry with any employees, it is required to carry workers’ compensation coverage under Alabama law.

What happens if a business in Alabama doesn’t comply with insurance requirements?

Non-compliance can result in fines of up to $1,000 per day per uncovered employee and potential suspension of the business license by the Alabama Department of Insurance.

Are personal auto policies valid for business vehicle use in Alabama?

No, personal auto policies don’t cover vehicles used for business purposes. Alabama law requires separate commercial auto insurance for company vehicles.

What insurance do Alabama contractors need?

Contractors typically need workers’ compensation, general liability, commercial auto, and possibly builders’ risk or professional liability insurance, depending on the services offered.

How can Alabama businesses save on required insurance coverage?

Businesses can save by bundling policies, maintaining effective risk management programs, responsibly raising deductibles, and working with independent agents to compare carrier options.

Sources

Alabama Department of Labor, “Workers’ Compensation Enforcement Guidelines.” – Title 25, Chapter 5, Alabama Administrative Code.

Alabama Department of Insurance, “2024 Enforcement Actions Report,” aldoi.gov. – October 2024.