Some people want personalized attention, while others prefer the consistency of sticking with one provider. It is helpful to understand how each agent type operates in practice.

Alabama’s insurance market is always shifting, and understanding both types puts you in the driver’s seat.

What Are Independent Insurance Agents?

Independent insurance agents are licensed professionals who help individuals and businesses find coverage by working with multiple insurance companies.

Since they aren’t tied to just one carrier, they can offer more quotes, more options, and more control over policy choices and pricing.

Independent Agent Definition & Legal Status

An independent agent is a licensed insurance expert who can legally sell policies from several insurance companies. Unlike captive agents, who are typically tied to one company, independent agents work for themselves or independent agencies.

They sign contracts with multiple insurers but don’t work as direct employees. These agents have to follow state and federal laws.

In Alabama, individuals must have an active insurance license, complete continuing education requirements, and act in the best interest of their clients.

Their legal duty is to give accurate info, show all reasonable coverage options, and avoid conflicts of interest.

Insurers pay independent agents commissions for the products they sell. If you ask, they should be able to tell you about this. State insurance law and their contracts with insurers lay out their role.

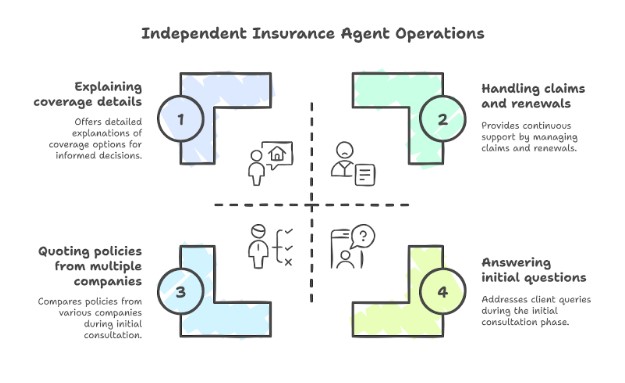

How Independent Agents Operate

Independent agents start by learning about the client’s insurance needs, budget, and risks. Then they compare policies and prices from several providers.

They don’t have to favor any single insurer, so they can show you competing options and explain the pros and cons of each. When you’re ready to buy, the agent helps fill out applications, explains policy terms, and answers questions.

After the sale, independent agents usually handle customer service, renewals, claims questions, and policy changes for their clients. Key activities include:

Quoting policies from multiple companies

Explaining coverage details and exclusions

Helping clients file claims and resolve problems

Keeping up with changes in insurance laws

Independent Agent Business Model

Independent insurance agents build their business on offering choices. That flexibility is what sets them apart.

They earn commissions from insurers for every policy sold or renewed, typically ranging from 10% to 20% of the premium. The actual rate depends on the type of insurance and the insurer.

Most independent agents run their agencies or work in local or regional agencies. They take care of their own office costs, marketing, and staff.

Since they’re not tied to one company, they must maintain good relationships with several insurers and stay up-to-date on new products and rates. Customer service matters a lot because they count on repeat business and referrals.

The Insurance Information Institute’s 2024 market analysis found that consumers using Independent agents who compared quotes from multiple carriers achieved average savings of 23% compared to single-carrier purchases¹.

In Alabama specifically, the Alabama Independent Insurance Association’s 2024 member survey indicated average savings of 19% for consumers who switched from captive to independent agents².

Alabama Independent Agent Requirements

In Alabama, independent agents must meet specific requirements to operate legally. First, they need to get an insurance producer license by passing a state exam.

After licensing, they must complete continuing education to stay up-to-date with changes and new information. Alabama law also requires agents to be transparent about their compensation and to adhere to ethical guidelines.

They must give clear, accurate info and can’t mislead customers. Agents must also follow rules for handling personal information and client money.

Key Alabama requirements:

Be at least 18 years old

Complete pre-licensing and continuing education

Pass background and licensing checks

Follow ethical standards set by the Alabama Department of Insurance

What Are Captive Insurance Agents?

Captive insurance agents represent just one insurance company. Their job centers on promoting the rates and products of that single insurer, which can affect pricing and options for customers.

Captive Agent Definition & Constraints

A captive insurance agent sells insurance only for one parent company. They can’t offer policies from any other brands, even if another company has better pricing.

This loyalty to a single provider shapes their entire job. Captive agents must follow strict rules set by their parent company, which cover sales methods, types of policies, and the handling of claims.

The company might give them a steady paycheck or provide insurance leads, but agents lose the flexibility to shop outside their assigned brand.

Key constraints of captive agents:

Must follow only one insurer’s product lineup

Cannot compare or sell competitor policies

Supervised by their company on how to handle customers

Tied to the rules and goals set by corporate management

Their primary responsibility is to grow business for their single insurer, rather than comparing offers among several carriers for each client.

How Captive Agents Operate

Captive agents rarely run their own business. Most work as employees or exclusive contractors for a big insurer.

The company typically provides them with training, marketing materials, and occasionally an office. Most captive agents are compensated through a combination of salary and commissions, or both.

Some earn bonuses based on the number of policies they sell. Since the company supports them, agents spend more time selling and less time on admin work.

Daily operations for captive agents often include:

Meeting with customers to discuss needs

Quoting only the rates and products of their insurer

Submitting applications and claims through their own company’s systems

Focusing on insurance lines like auto, home, or life favored by the carrier

Captive agents receive direction and oversight, which helps maintain consistency in policies and service.

Captive Agent Limitations

One significant drawback of captive agents is the limited choice. They can only show you policy options from their own company.

If a competitor has lower rates or better coverage, captive agents can’t recommend or sell it. This makes price competition tough and sometimes means customers don’t get the best deal.

Captive agents may be incentivized to sell more of certain products, causing them to focus on meeting company sales targets. Unlike independent agents, they can’t compare rates from multiple insurers or build solutions from a wide market.

Customers who want numerous options may not receive the most competitive or personalized results from a captive insurance agent.

Looking for reliable home insurance options in Alabama? Woodall & Hoggle Insurance Agency helps you review multiple policies side by side, allowing you to make informed choices. Contact us to get started.

If you’re ready to get

started, call us now!

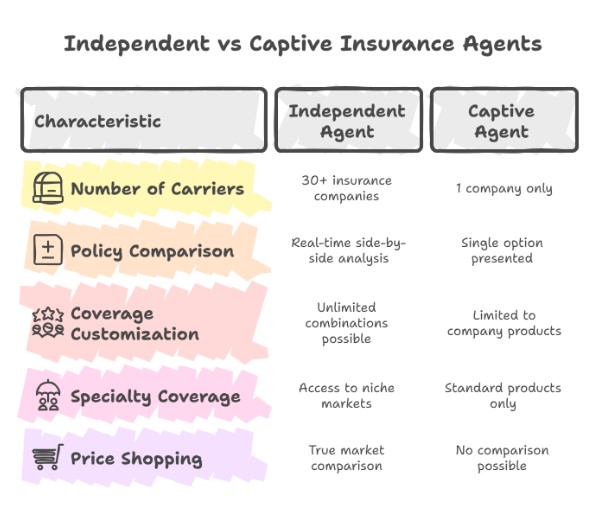

Side-By-Side Comparison: Independent vs Captive

Picking the right insurance agent can significantly impact the level of choice, support, and value you receive. The differences between independent and captive agents show up in coverage options, service, expertise, and pricing.

Choice And Coverage Options

Comparison Factor

Independent Agents (Woodall & Hoggle)

Captive Agents

Number of Carriers

30+ insurance companies

1 company only

Policy Comparison

Real-time side-by-side analysis

Single option presented

Coverage Customization

Unlimited combinations possible

Limited to company products

Specialty Coverage

Access to niche markets

Standard products only

Price Shopping

True market comparison

No comparison possible

Service And Advocacy

Service Factor

Independent Agents

Captive Agents

Claims Advocacy

Represents YOUR interests

Represents company interests

Coverage Reviews

Multi-carrier alternatives suggested

Company products only

Problem Resolution

Multiple solutions available

Limited to company policies

Long-term Planning

Client-focused strategy

Company-directed priorities

Expertise And Market Knowledge

Independent agents typically gain experience with a broader range of insurance products and companies. They keep up with market changes, new offerings, and regulatory updates.

This makes them a reliable resource for clients with unique needs or those seeking the latest coverage options. Captive agents focus on their company’s products and guidelines.

Their expertise runs deep, but only for their brand. They are familiar with their company’s plans inside and out, but may not be as well-versed in competitors’ products or the broader market.

Customers who require a comprehensive view or wish to compare companies may appreciate the expertise of an independent agent.

Cost And Value Analysis

Independent agents compare prices from several insurance companies to find competitive rates. This can lead to savings on home, auto, and life insurance policies.

Clients often get better deals, especially when bundling coverage or seeking discounts that aren’t tied to just one company.

Captive agents usually offer set prices and packages from a single carrier. Sometimes you’ll get special deals or loyalty perks, but there’s less room to shop for lower premiums or broader coverage.

Price checking and negotiation are less flexible with captive agents.

Alabama-Specific Considerations

Alabama’s insurance landscape brings its own set of challenges for both independent and captive agents. Factors like local competition, legal requirements, and regional hazards all shape insurance needs.

Alabama Insurance Market Dynamics

National and regional carriers compete alongside a strong network of independent agents in Alabama. The state has seen independent agencies grow as people want flexible policy options and local guidance.

In many Alabama towns, independent agents work with multiple insurance companies. This lets them offer a wide range of policy choices to customers.

Captive agents typically represent large national brands and specialize in a specific range of insurance products.

Alabama’s agricultural sector and urban growth have created varied insurance needs. Small businesses often turn to independent agents for packages tailored to local risks and needs.

Home and auto insurance are top sellers due to the threat of tornadoes and hurricanes.

Both independent and captive agents have to meet strict education and licensing requirements. ALDOI updates regulations to reflect industry trends, such as disaster readiness and market accessibility.

Agents follow state guidelines when explaining coverage and helping individuals make informed decisions. State laws also shape how rates are set, especially for property insurance in coastal or storm-prone areas.

All agents must renew licenses every two years

Continuing education is required for license renewal

Agencies must stay current with regulatory changes to serve their customers effectively.

Regional Carrier Considerations

Alabama has several regional insurers focused on state-specific needs. Independent agents often partner with these local carriers, offering more options for unique risks, such as mobile home or farm insurance.

Captive agents typically remain with national companies and often have fewer local options. This can impact product availability and customization for customers residing in areas outside major cities or in rural regions.

Independent agents adapt quickly when regional carriers enter or leave the market. Their customers are less likely to lose coverage options, which gives Alabama families and businesses more stability.

Geographic Risk Factors

Alabama faces unique risks, with tornadoes, hurricanes, and flooding being common threats to homes and businesses.

Agents need to understand local weather patterns, flood zones, and wildfire risk. Independent agents compare products from several carriers to help consumers get better protection against these hazards.

Captive agents may be required to adhere to pre-set policies, which can limit their choices for individuals in high-risk or unusual locations.

Communities near the Gulf Coast, the Tennessee Valley, and rural areas each deal with different exposures. Coastal counties must consider hurricane deductibles and windstorm policies, while northern Alabama faces higher risks of tornadoes.

Risk Highlights Table

Region

Key Risk Factors

Common Coverage Needs

Gulf Coast

Hurricanes, Flooding

Windstorm, Flood

Central Alabama

Tornadoes, Severe Storms

Home, Auto, Roof Coverage

Rural Areas

Fire, Hail, Crop Loss

Farm, Crop, Fire

When To Choose An Independent Agent

Independent insurance agents offer clients a wider range of policy choices and more flexible service.

Their market access enables Alabama buyers to tailor insurance to their unique needs, changing situations, and cost efficiency.

Ideal Scenarios For Independent Agents

Independent agents are a good fit for people who want coverage from several companies, not just one. Families with homes, cars, and boats often find it easier to combine their various policies through a single agent.

Multi-state property owners benefit since independent agents compare options from many providers. This often means coverage that fits different lifestyles or risk profiles.

Major life events—like marriage, home purchase, or starting a business—often require insurance that a single company can’t always supply.

Independent agents quote across many carriers to match the right coverage to each situation.

Professional And Business Considerations

Business owners should consider independent agents if their operations are exposed to unique risks. A captive agent may only offer standard options from one carrier.

Independent agents can find policies tailored to meet industry-specific needs. Professionals, such as doctors, lawyers, or contractors, often require highly customized liability coverage. Independents research multiple insurers for tailored solutions and better pricing.

New businesses, especially in industries with changing regulations, benefit from the flexibility independents provide.

They can quickly shift coverage as business needs evolve without locking clients into one company’s products.

Financial Optimization Scenarios

Cost-conscious consumers often turn to independent agents to compare prices and maximize value. When bundling home, auto, and other personal policies, independents frequently spot combinations that lower overall premiums.

People with claim histories or specialized insurance needs—like antique car collectors or high-value homeowners—may find lower rates with lesser-known carriers represented by independent agents.

Independent agents help clients find discounts not available through captive providers. Their access to multiple companies encourages price competition, making it easier for clients to manage budgets while still getting strong protection.

Alabama-Specific Independent Agent Benefits

Alabama’s insurance market includes both national brands and regional carriers. Independent agents often work with local insurers who understand Alabama’s weather risks, coastal exposure, and community needs.

Clients near the Gulf Coast or in areas prone to tornadoes often require specialized coverage for flood or storm damage. Independent agents can pinpoint regional carriers with experience insuring these risks, something captive agents tied to national chains may not offer.

Alabama residents facing unique local regulations or industry trends get direct support from agents with deep area knowledge.

Choosing auto insurance in Alabama doesn’t have to be confusing. Let Woodall & Hoggle Insurance Agency help you find the right fit with one easy quote request. Schedule a call now.

If you’re ready to get

started, call us now!

When Captive Agents Might Work

Captive insurance agents can be a logical fit in some situations. Their role suits clients who want simplicity or strong guidance over a wide range of choices.

Simple Insurance Scenarios

A captive agent can be the right match when someone’s insurance needs are straightforward. Drivers looking for standard auto coverage or homeowners with a single property often find that a captive agent offers everything needed for basic protection.

Captive agents usually know their company’s main products inside and out. If you don’t need specialty coverage or bundled services, you might benefit from that expertise.

In these cases, the limited menu of policies isn’t a problem. Routine policies, like basic liability or auto, tend to be similar across companies.

For many Alabama families, a single provider can be sufficient when coverage needs are straightforward and uncomplicated.

Decision-Making Preferences

Some people prefer a hands-off insurance shopping experience and opt for a captive agent’s process. These agents often give direct recommendations based on their company’s offerings.

Some policyholders feel more comfortable trusting an agent’s guidance instead of comparing lots of companies and plans. The decision is easier because there are fewer options to sort through.

With captive agents, follow-up and changes are usually simple. A captive agent can feel more like a personal advisor when making choices.

For customers who value quick, clear guidance over comparing rates from multiple carriers, this approach may save time and stress.

Captive Agent Advantages (Limited)

Captive agents get support from established insurance brands. These brands usually offer local offices, recognizable names, and solid customer service systems.

Training for captive agents tends to be robust. They often get deep education on their company’s policies and claims process, which can lead to consistent, dependable service.

Some companies back their captive agents with digital tools and 24/7 claim hotlines. If you prioritize brand familiarity, streamlined claims, and want in-person help, captive agents can meet those needs.

Limitations To Consider

There are downsides—captive agents can’t offer policies from multiple insurance companies. Clients are often limited to what one company provides, which may not always meet their unique or changing needs.

A captive agent can’t compare rates or coverage options across competitors. This can lead to higher costs or missing out on features that other providers offer.

If a client’s needs become more complex or they wish to compare specialized products, an independent agent may be a better fit. It’s worth weighing these limitations when deciding between an independent and captive agent.

How To Evaluate Insurance Agents In Alabama

Choosing an insurance agent can impact coverage, service, and price. The best decision comes from asking clear questions, checking credentials, and watching for important warning signs.

Essential Questions For Any Agent

Clients should ask direct questions to judge an agent’s skill, trustworthiness, and fit. Try these:

How many insurance companies do you work with? This indicates whether the agent offers a range of choices or just one.

Do salary, commission, or both pay you? This can affect advice.

How do you help clients when they have to file a claim? Good agents stand by clients.

Can I see your insurance license and proof of continuing education? Alabama requires agents to finish 24 hours of education every two years to keep their knowledge current.

Why did you recommend this policy over others? Honest agents give clear reasons, not just prices.

Creating a quick list of questions helps you compare agents and determine who is most helpful and transparent.

Independent Agent Evaluation Criteria

Independent agents typically work with a greater number of insurance companies than captive agents. When you’re checking them out, keep these points in mind:

Company Selection: Do they represent several respected insurers?

Personalized Service: Are they tailoring coverage to your actual needs, or just selling on price?

Claims Advocacy: Will they step in if you have a dispute with your insurer?

Experience: How long have they been around, and what credentials do they have?

Community Reputation: Are people saying good things? Membership in groups like the Alabama Independent Insurance Agents typically indicates a commitment to ethics and staying current with the industry.

Good independent agents give you more choices and act as advisors, not just salespeople.

Red Flags To Avoid (Any Agent Type)

Some warning signs just can’t be ignored. Watch out for these:

Pushing only one or two products without giving reasons.

Dodging your questions or refusing to provide anything in writing.

High-pressure sales tactics or demands for a quick decision.

No physical address, bad communication, or missing state license.

Lack of continuing education, which Alabama requires.

Reports of past disciplinary actions or unethical behavior.

If an agent can’t explain policy differences or won’t give clear cost comparisons, that’s a problem. Honestly, it’s smart to walk away if you see these red flags.

Alabama-Specific Verification

Every Alabama insurance agent is required to hold a state license. They must meet educational requirements and adhere to clear standards.

Here’s how you can check:

Ask for their Alabama insurance license number and look it up on the state insurance department’s website.

Ensure they’ve completed the 24-hour continuing education requirement every two years, as mandated by Alabama law.

Double-check that their contact information—address, phone number, and email—matches what is listed on the official agency websites.

Making Your Decision: Alabama Agent Selection Framework

Choosing the right insurance agent in Alabama comes down to understanding your own needs, your business goals, and how local rules work.

Independent and captive agents each have their perks, depending on what you want—service, flexibility, or a certain kind of coverage.

Decision-Making Process

Start by getting honest about your coverage needs and expectations. If you run a business with complicated insurance requirements, you might need the flexibility of an independent agent.

On the other hand, if you want something straightforward, captive agents can offer specialized products from one insurer. There’s no shame in liking things simple.

It helps to build a checklist. Think about your business or household’s size and risk, Alabama’s unique factors, and how much personal attention you want.

Balance cost, service, and whether you want a wide range of policy choices or something more focused.

Gather a list of agent candidates and check their licenses with the Alabama Department of Insurance. See which agencies they work with, what clients are saying, and how many policy types they handle.

If you’re considering independent agents, ask how many insurance carriers they represent and if their advice feels unbiased.

For captive agents, focus on their expertise with their company’s products and their customer service track record.

Set up a quick call or meeting. Request sample quotes for similar coverage and observe how they present your options.

It’s helpful to create a side-by-side chart comparing the pros and cons. For example:

Factor

Independent Agent

Captive Agent

Carrier Options

Multiple insurers

Single company

Policy Flexibility

Usually higher

Lower

Pricing

Competitive, varies

Company set pricing

Expertise

Broader, but less deep

Deep in one company

Questions To Ask Yourself

What’s my main priority—price, flexibility, or personal service?

Do I want to compare several insurance carriers, or stick with just one?

Do I need special coverage for auto, home, or business?

How much does local Alabama know-how matter to me?

Am I hoping for a long-term relationship with one agent, or do I prefer to shop around?

It’s easy to get distracted, so these questions keep you focused. Taking a minute for self-assessment makes agent meetings way more productive.

Woodall & Hoggle’s Independent Advantage

Woodall & Hoggle stands out in Alabama with their independent approach to insurance.

Their model offers more choices, flexible coverage, and a personal touch that you don’t always get from captive agencies.

Unique Market Position

They’re not tied to just one company. Instead, Woodall & Hoggle can offer products from several top carriers, allowing clients to choose options that suit their budgets and situations.

Being independent means they can adapt quickly to what’s happening in Alabama. If home values shift or auto risks change, they don’t have to wait for a head office to approve anything.

Unlike captive agents, who are often limited to a single menu, Woodall & Hoggle compare multiple policies at once. That usually means better rates and coverage for their customers.

Clients can sit down, review the options, and make informed choices with advice that’s not influenced by company quotas.

Proven Track Record

Woodall & Hoggle has decades of experience serving the state of Alabama. They’ve built a reputation for dependable service and have earned repeat business from families and businesses across the state.

Customer testimonials and reviews mention their fast claims support and detailed policy reviews. People seem to appreciate how they walk you through every step—no rushing, no confusion.

Industry awards and local recognition back up their claims of quality. Their stability gives clients peace of mind, knowing that someone will be there for them in the future.

Service Differentiation

Woodall & Hoggle go beyond the basics. They offer a wide range of insurance—from homeowners and auto to business and life—so clients can get everything in one place.

You get a dedicated team, not a faceless call center. Their agents remember what you need and reach out before renewals or big life changes.

They utilize modern technology for digital quotes and claims, but you still receive genuine local support. It’s a good mix—easy online access and someone who understands the Alabama market when you need it.

Woodall & Hoggle Insurance Agency makes comparing business insurance policies simple, fast, and transparent across 30+ top-rated carriers. Ready to protect your company more confidently? Contact us today.

Contact Us Today For An Appointment

Frequently Asked Questions

What is the difference between independent and captive insurance agents?

Independent agents work with multiple insurance carriers and can offer a range of quotes and coverage options. Captive agents represent only one insurance company and sell its products exclusively.

Are independent insurance agents cheaper in Alabama?

Yes, independent agents in Alabama often help clients save money by comparing policies across multiple insurers. This can result in lower premiums and more tailored coverage compared to quotes from a single carrier.

Is it better to use an independent or captive agent?

Independent agents offer more flexibility and options, making them ideal for shoppers who want to compare rates and find the best deals. Captive agents may possess more in-depth expertise on a company’s products but often lack competitive quoting capabilities.

How do insurance laws affect agents in Alabama?

Alabama law requires all agents, whether independent or captive, to be licensed and comply with strict coverage, disclosure, and continuing education requirements. Violations can lead to fines or license suspension.

Can independent agents help with both personal and business insurance?

Yes, most independent agents in Alabama offer both personal (auto, home, and life) and commercial (liability, workers’ compensation, and property) insurance solutions, making them a one-stop shop for comprehensive coverage.

Why do Alabama businesses prefer independent agents?

Many Alabama businesses choose independent agents for their ability to compare policies, offer competitive pricing, and tailor coverage to industry-specific risks, such as storm damage, liability, and workers’ compensation.

Legal Resources

National Association of Insurance Commissioners, “2024 Consumer Insurance Survey.” – NAIC.org, March 2024.

Alabama Department of Insurance, “2024 Consumer Education and Market Report.” – aldoi.gov, September 2024.