Originally published: April 2023 | Updated: December 2025

Alabama faces serious flood risks that often catch homeowners off guard. Alabama is one of the most flood-prone states in the U.S., with thousands of properties at risk each year from coastal storms, heavy rains, and river flooding.

Many people only realize too late that their standard home insurance doesn’t cover flood damage. That’s a harsh lesson, and it’s more common than you’d think.

Flood insurance protects Alabama homeowners from financial disaster when flooding strikes, but coverage requirements and costs can vary a lot depending on where you live and your specific risk factors.

The good news? Both government-backed and private options exist, so you’ve got choices when it comes to protection.

Flood insurance premiums keep rising in Alabama. Some areas have seen costs double under new pricing methods.

Knowing what’s available and how to get the right coverage could save you money—and stress. It’s really about understanding when you need coverage, what it includes, and how to actually buy it without headaches.

Key Takeaways

Regular homeowners’ insurance doesn’t cover flood damage, so separate flood insurance is essential in Alabama.

Both government NFIP and private flood insurance are available, each with different coverage levels and pricing.

Flood insurance costs can be all over the map, but a smart evaluation helps you find something affordable that actually protects you.

Do Alabama Homeowners Need Flood Insurance?

No, Alabama doesn’t legally require homeowners to have flood insurance. That said, lenders might insist on it depending on your situation.

Woodall & Hoggle helps Alabama homeowners understand their real flood exposure and compare coverage options that fit their budget. Protect your home with confidence today. Contact us.

If you’re ready to get

started, call us now!

Understanding Flood Insurance In Alabama (NFIP Vs Private Options)

Alabama homeowners really have two main choices: the National Flood Insurance Program or private insurers.

NFIP is backed by the federal government, while private companies often offer higher limits and broader coverage.

What NFIP Covers, Limits, And Eligibility

The National Flood Insurance Program sets out standardized coverage for homes and businesses. NFIP covers up to $250,000 for your house and $100,000 for personal property.

NFIP policies cover the structure, foundation, electrical, plumbing, and built-in appliances. For your stuff, it covers furniture, clothing, and portable appliances.

You buy NFIP coverage through licensed agents. If your property’s in a participating community, you’re eligible—it doesn’t matter if you’re in a high or low risk zone.

Key NFIP features:

Fixed coverage limits

30-day waiting period for new policies

Federal backing means NFIP plans stick around, even if private companies pull out

Standard deductibles start at $1,000

How Private Flood Insurance Differs (Limits, Add-Ons, Pricing)

Private flood insurance usually offers higher limits and more coverage options than the NFIP. Some private policies will go up to $10 million or even more.

Private insurers often include extra living expenses if you have to move out during repairs. Some will even cover basement upgrades, pool damage, and landscaping—stuff NFIP skips.

Prices really depend on the company and your property. Newer, well-kept homes in safer areas usually get the best deals.

Private insurance advantages:

Much higher coverage limits

Extra living expenses if you’re displaced

Replacement cost options

No waiting period with some insurers

Flexible deductibles

Which Type Works Best For Different Property Situations

High-value homes really need private coverage with higher limits and replacement cost coverage. If your place is worth more than $250,000, private insurance helps you avoid coverage gaps.

Homes in high-risk zones might find NFIP more affordable, especially if the house is older and private quotes are sky-high. NFIP provides a baseline of coverage, often at a more stable price.

New builds and well-maintained homes often get better private rates and beefier coverage. Insurers see them as less risky.

Investment properties and businesses usually choose private insurance for higher limits and faster claims. The higher premium can be worth it if you’re protecting rental income or business property.

You should compare both options every year—private flood insurance availability varies by your area and property details.

How To Evaluate Your Flood Risk In Alabama

Alabama property owners can determine their flood risk by checking FEMA flood maps, obtaining elevation certificates, reviewing local drainage, and examining historical flood data.

Two thousand twenty-five flood risk data for Alabama shows a 15% increase in properties at risk across the state.

Using FEMA Flood Maps (FIRM) For Zone Identification

FEMA’s Flood Insurance Rate Maps (FIRM) lay out the flood zones for Alabama. These digital maps break down risk areas all over the state.

Homes built above the BFE often receive significant discounts. If your place sits below the BFE, expect higher premiums—it’s just riskier.

Get a current elevation certificate when you’re buying flood insurance. Old ones might not reflect new maps or renovations.

Local Drainage, Climate Trends, And Historical Flood Data

Local drainage can make or break your flood risk, and FEMA maps don’t always catch those details. Inadequate drainage means flooding can happen even in “safe” zones.

Take a look at nearby storm drains, ponds, and streams. If they’re blocked or undersized, flooding gets worse during heavy rain.

Climate factors that matter in Alabama:

Hurricane season (June–November)

Spring storms

How saturated the soil is

More pavement and buildings, which means less absorption

Old flood records can reveal patterns that current risk maps miss. Local emergency management keeps databases of past flood events.

New developments are changing drainage in many Alabama communities. Sometimes, new construction pushes water toward areas that used to be safe—so it’s worth keeping an eye on what’s happening nearby.

The National Flood Insurance Program bases premiums on several key factors that directly impact what Alabama homeowners pay.

Flood zone designation is the primary cost driver, with high-risk zones carrying substantially higher premiums than moderate- or low-risk areas.

Property elevation plays a crucial role in determining rates.

Homes built above the Base Flood Elevation usually qualify for lower premiums, while properties below this level face much higher costs.

Structure characteristics also influence pricing:

Foundation type (slab, crawl space, basement)

Number of floors

Age of construction

Building materials used

Deductible selection lets homeowners control their premiums.

Higher deductibles lower annual costs but increase out-of-pocket expenses at the time of a claim.

The building’s occupancy type also affects rates. Primary residences typically cost less to insure than secondary homes or rental properties.

Typical Premium Ranges For Inland & Coastal Areas

Alabama’s diverse geography creates significant premium variations across the state.

Coastal counties along the Gulf of Mexico face the highest rates of damage due to hurricane and storm-surge risks.

Coastal Premium Ranges:

High-risk zones: $2,000 – $4,000+ annually

Moderate-risk zones: $800 – $1,500 annually

Low-risk zones: $400 – $800 annually

Inland Premium Ranges:

High-risk zones: $1,200 – $2,500 annually

Moderate-risk zones: $500 – $1,000 annually

Low-risk zones: $200 – $600 annually

River communities and areas prone to flash flooding may see rates similar to coastal moderate-risk zones.

FEMA’s updated pricing methodology continues pushing premiums higher, with some areas expected to see rates double.

Properties in Birmingham, Montgomery, and other inland cities usually fall into lower premium ranges unless they’re near waterways or in known flood-prone areas.

How Private Market Pricing Differs

Private flood insurance operates under different rules than the NFIP.

Private insurers often deliver more competitive rates for certain properties by using advanced risk modeling and skipping federal rate restrictions.

Private insurers often offer lower premiums for homes in moderate and low-risk areas.

They can price more accurately using detailed flood models and property-specific data.

Coverage differences include higher dwelling limits and additional living expense coverage.

Private policies may cover basements and other areas the NFIP excludes.

However, private market pricing can exceed NFIP rates for high-risk coastal properties.

Homeowners should compare both options to find the most suitable coverage and pricing for their specific situation.

Private insurers also consider credit scores and claims history in their pricing, factors that the NFIP doesn’t use.

Get personalized guidance from Woodall & Hoggle as you review NFIP and private flood insurance choices tailored to your property’s risk. Make informed decisions with ease. Schedule an appointment.

If you’re ready to get

started, call us now!

What Flood Insurance Covers — And What It Doesn’t

Flood insurance covers two main categories: building damage and personal belongings, each with specific limits and exclusions.

Understanding these coverage gaps helps Alabama homeowners make informed decisions about protecting their property from flood damage.

Building Coverage Basics (Foundation, Electrical, HVAC)

Building coverage protects the physical structure of your home and permanently installed systems.

This includes your foundation, walls, floors, and roof up to your policy limit.

Covered Building Elements:

Foundation and structural supports

Electrical and plumbing systems

Central air conditioning equipment

Furnaces and water heaters

Built-in appliances like dishwashers

Permanently installed carpeting over unfinished floors

The electrical system coverage includes wiring, outlets, and circuit breakers.

HVAC systems receive full protection when they’re permanently installed and part of the building structure.

Coverage typically maxes out at $250,000 for residential buildings.

This amount covers repair or replacement costs for covered building components damaged by flood waters.

Contents Coverage & Important Limits

Contents coverage protects your personal belongings inside the home.

Flood insurance contents coverage requires a separate policy endorsement and has strict limits.

Covered Personal Property:

Furniture and clothing

Electronics and appliances

Artwork and collectibles (with limits)

Food and medicine

Portable air conditioners and microwaves

Important Monetary Limits:

Maximum contents coverage: $100,000

Artwork limit: $2,500 per piece

Jewelry limit: $2,500 total

Furs limit: $2,500 total

Contents coverage pays actual cash value, not replacement cost.

This means depreciation reduces your payout amount.

Common Exclusions (Sewer Backup, Earth Movement, Basement Items)

What flood insurance doesn’t cover often surprises homeowners.

These exclusions can leave significant gaps in protection.

Major Exclusions Include:

Sewer backup damage (unless caused by flooding)

Earth movement, such as landslides or sinkholes

Currency, precious metals, and important papers

Cars, boats, and RVs

Swimming pools and fences

Landscaping and outdoor equipment

Basement Coverage Restrictions:

Finished basement areas get minimal coverage. Only basic structural elements qualify for building coverage.

Personal property in basements is subject to strict limitations. Items like basement furniture, electronics, and stored belongings are usually not covered by the lowest elevated floor.

Optional Endorsements Worth Considering

Standard flood policies offer basic protection, but endorsements can fill important coverage gaps.

These additions cost extra but provide valuable protection for specific situations.

Increased Cost of Compliance (ICC):

Covers up to $30,000 for building upgrades required by local flood ordinances after damage.

This helps pay for elevating your home or other required improvements.

Replacement Cost Coverage:

Upgrades contents coverage from actual cash value to replacement cost.

This eliminates depreciation deductions from your claim payments.

Basement Improvements Coverage:

Some insurers offer limited endorsements for finished basement areas. Coverage remains restricted but provides better protection than standard policies.

These endorsements vary by insurance company and may not be available in all areas.

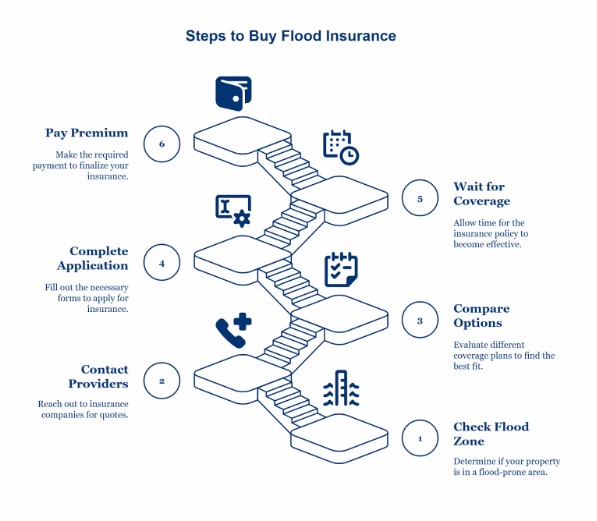

Step-By-Step: How To Buy Flood Insurance In Alabama

Buying flood insurance in Alabama requires following a clear process.

Most homeowners can choose between private carriers or the National Flood Insurance Program (NFIP).

Step 1: Check Your Flood Zone

Property owners should first determine their flood zone designation. This information affects coverage options and pricing.

Step 2: Contact Insurance Providers

Residents can contact licensed insurance agents who offer flood coverage. Alabama flood insurance providers offer both private and NFIP options.

Step 3: Compare Coverage Options

Option

Benefits

NFIP

Government-backed, standardized rates

Private Insurance

Flexible coverage, competitive pricing

Step 4: Complete the Application

Insurance agents help property owners fill out application forms. They provide guidance on coverage amounts and policy details.

Step 5: Wait for Coverage to Begin

Flood insurance policies typically have a 30-day waiting period before coverage starts. Emergencies may allow for shorter waiting periods.

Step 6: Pay Your Premium

Property owners must pay their first premium to activate coverage—premium costs in Alabama range from $927 to $2,051, depending on risk factors.

Insurance agents can help homeowners navigate the entire process. They make sure you select the right coverage and handle all the paperwork.

If you’re ready to get

started, call us now!

What Happens When NFIP Is Delayed Or Unavailable?

The National Flood Insurance Program sometimes experiences delays or lapses, leaving Alabama homeowners without access to federal flood coverage.

During these periods, the NFIP cannot issue new policies or renew existing ones.

When the NFIP lapses, immediate restrictions hit Alabama. The program can’t issue new flood insurance policies during a government shutdown.

Existing policies stay active if issued before the lapse date. But homeowners can’t renew expiring policies during the gap.

New homebuyers run into the biggest headaches. They can’t get NFIP coverage to meet mortgage requirements.

This leads to delays in closing dates and financing approvals.

Key impacts include:

New applications – Completely suspended

Policy renewals – Can’t be processed

Active policies – Stay valid until expiration

Claims processing – Might get delayed

Property owners should double-check their policy status before any lapse. If your policy expires during a gap, you’ll need to find other coverage quickly.

When Private Flood Insurance Becomes The Only Option

Private flood insurance steps in when NFIP isn’t available. Alabama homeowners can buy policies from private insurers without waiting for the federal program to come back online.

Private policies sometimes offer better coverage than NFIP—some cover basement improvements, extra living expenses, or higher overall limits.

Processing times usually move faster, too.

Advantages of private coverage:

Available during NFIP lapses

Higher coverage limits

More comprehensive protection

Faster claim processing

Potential drawbacks:

Higher premiums in some areas

Stricter underwriting requirements

Limited availability in high-risk zones

It’s smart to compare a few private insurers. Prices and coverage can really swing from one company to another.

Real Estate Transactions During NFIP Gaps

NFIP lapses seriously complicate real estate deals in Alabama. NFIP’s authority to provide flood insurance is currently set to expire at midnight on January 30, 2026, which could mess with pending sales.

Mortgage lenders require flood insurance for homes in Special Flood Hazard Areas. If NFIP isn’t available, buyers must obtain private coverage or face closing delays.

Real estate agents need to get clients ready early. They should help buyers find private insurance options before any NFIP gap happens.

Transaction impacts:

Delayed closings – Pretty common when coverage gaps exist

Higher costs – Private insurance often costs more

Limited options – Fewer insurers in high-risk areas

Contract complications – Insurance contingencies can fall through

Buyers should start the insurance process as soon as the contract is signed. That gives them time to line up private coverage if NFIP isn’t available.

Sellers can make things easier by sharing flood zone documents and past insurance info. That speeds up private insurance applications a lot.

Filing A Flood Insurance Claim In Alabama

Filing a flood insurance claim means you need to act fast and gather the right paperwork. Alabama residents must follow specific steps, whether they use NFIP or private flood insurance.

Immediate Steps To Take After Flood Damage

Call your insurance agent or company right after flood damage happens. Most policies want you to notify them within 60 days of the loss.

Take photos and videos of the damage before you start cleaning up. Get shots from different angles—show water lines on walls and any ruined stuff.

Safety comes first:

Don’t enter flooded areas until authorities say it’s safe

Turn off electricity and gas if water reaches the outlets

Wear protective gear when checking damage

Make temporary repairs to stop more damage. Keep all receipts for emergency fixes and temporary housing.

Filing a flood insurance claim in Alabama means knowing the legal steps to get the right payout.

Documentation Needed For NFIP Or Private Claims

Keep detailed records of everything damaged and the cost of repairs. Make an inventory list with descriptions, when you bought each item, and what you think it’s worth.

Required documentation includes:

Policy number and contact info

Photos of all damaged areas and belongings

Receipts for emergency repairs and living expenses

Inventory of damaged personal property

Any previous flood damage records

Sort damaged items by type—structure, personal belongings, or business equipment. Don’t toss anything until the adjuster checks it out.

The agency brings more than 150 years of combined training and experience to help homeowners find the right coverage. That’s a lot of know-how under one roof.

They partner with several insurance companies to offer competitive rates and a range of coverage options. You get more choices, not just a one-size-fits-all policy.

Key Services Include:

Flood insurance through private carriers and NFIP programs

Homeowners insurance for houses, condos, and rentals

Commercial insurance for business properties

Free quotes with personalized guidance

Woodall & Hoggle really digs into flood insurance solutions for Alabama families.

Their agents know standard homeowners’ policies usually don’t cover flood damage, which can catch folks off guard.

They focus on finding the right protection at the best rates. Every client’s situation is a little different, so they look at your specific needs and property risks.

The staff walks homeowners through the insurance process step by step. They explain coverage options and break down policy details so you’re not left guessing.

These folks keep up relationships with multiple insurance companies. That way, they can compare options and hunt down the best pricing for you.

The agency offers free homeowners insurance quotes with no obligation. They serve customers throughout the greater Guntersville and North Alabama region.

Secure reliable flood protection with Woodall & Hoggle and explore coverage options built around your Alabama home. Review your flood insurance needs now. Contact us.

Contact Us Today For An Appointment

Frequently Asked Questions

Does homeowners’ insurance cover flood damage in Alabama?

No. Standard homeowners’ insurance typically excludes flood damage. You need a separate NFIP or private flood insurance policy to protect your home and belongings from flood-related losses.

Do I need flood insurance if I’m not in a FEMA flood zone?

Yes, it’s recommended. Many damaging floods in Alabama occur outside high-risk zones, and a policy can still be purchased at a lower preferred rate.

How long does it take for flood insurance to begin?

NFIP policies generally require a 30-day waiting period before coverage starts, while private flood insurers may offer shorter waiting periods depending on the carrier.

What is the difference between NFIP and private flood insurance?

NFIP has standardized limits and pricing, while private flood insurance may offer higher coverage, flexible deductibles, and additional benefits. Comparing both helps you choose the best fit.

How much does flood insurance cost in Alabama?

Costs vary widely based on elevation, flood zone, foundation type, and coverage limits. Rates can range from a few hundred to several thousand dollars per year.

What does flood insurance typically cover?

Flood insurance usually covers the home’s structure, electrical systems, HVAC, built-ins, and personal belongings. Coverage varies by policy, so review building and contents limits carefully.

Can I switch from NFIP to private flood insurance?

Yes. Many Alabama homeowners move to private flood insurance for broader limits or competitive pricing, but always confirm lender acceptance before switching.