Tried and Tested Ways to Find the Best Homeowners Insurance in Huntsville, Alabama

Originally published: September 2023 | Updated: October 2025

Finding affordable homeowners insurance in Huntsville isn’t easy—premiums are among the highest in Alabama due to the risks of storms and rebuilding.

The city’s wild weather and unique housing market mean you’ve got to pay extra attention to your coverage choices.

To ensure accuracy, compare quotes from at least three insurers and verify your understanding of Alabama’s specific coverage requirements and available discounts.

Smart homeowners utilize proven strategies to obtain reliable protection at a fair price.

These methods help you avoid those annoying gaps in coverage or paying too much for stuff you don’t need.

Key Takeaways

Compare quotes from multiple insurers and consult with independent agents to find the best rates and coverage.

Know Alabama’s requirements and look closely at deductibles, flood insurance, and weather-related options.

Use discounts—bundle policies, upgrade your roof, install home security, whatever you can.

1- Compare at Least Three Local Quotes

Shopping multiple insurers is the single most effective way to find better rates in Huntsville. Independent agents can compare carriers for you at no extra cost.

Local and national carriers each have their own perks, and those can affect what you pay and the kind of service you get.

Why Huntsville Rates Differ by ZIP Code

Where you live in Huntsville changes your insurance costs. ZIP codes like 35801, downtown, usually cost more than those like 35803 in Jones Valley.

The weather makes a big difference. If you’re closer to the Tennessee River, you’ll pay more because of flood risk. Areas hit by more tornadoes in recent years see higher premiums—no surprise there.

Crime rates matter, too. Insurance companies review local police statistics, so if your ZIP code has a higher incidence of theft or vandalism, you’ll pay for it in your premium.

The age and type of your home also play a role. Older neighborhoods, especially those with homes from before 1980, often see higher rates. Those houses may not have updated electrical systems or storm-resistant roofs.

Local Carriers vs National Carriers

National carriers dominate the Huntsville market, offering the lowest average annual rates at $3,573. You receive steady pricing and a range of online tools for managing your policy.

Local carriers are more familiar with Alabama’s risks. They can pinpoint which Huntsville neighborhoods are most affected by hail or wind, so you may receive more accurate pricing for your specific situation.

National Carrier Benefits:

Lower average premiums

24/7 online claims

Lots of discounts

Coverage if you move out of state

Local Carrier Benefits:

More personal service

Faster local claims

Better at handling regional risks

Flexible coverage options

Independent agents can shop for both national and local carriers on your behalf. They’ll compare rates and help you pick what fits your needs best.

2- Check Alabama’s 2025 Coverage Requirements and Limits

Alabama doesn’t set home insurance minimums, but mortgage lenders require dwelling coverage. In 2025, Huntsville homeowners should prioritize replacement cost over ACV to protect against rising rebuild costs.

Understanding the difference between actual cash value (ACV) and replacement cost coverage, as well as extended replacement options, helps you select the right protection for your home’s value.

ACV vs Replacement Cost Explained

Actual Cash Value (ACV) pays what your stuff is worth now, minus depreciation. If your 10-year-old roof gets damaged, ACV coverage deducts a portion for wear and tear.

Replacement Cost pays whatever it takes to fix or replace with similar materials. It costs more, but you won’t get stuck footing a huge bill after a disaster.

Most folks in Huntsville do better with replacement cost coverage. Alabama storms and tornadoes can cause serious damage.

The price difference between ACV and replacement cost typically ranges from 10%-15% of your total premium. That bump in cost can save you thousands if you ever need to file a big claim.

Replacement cost works best for newer or recently renovated homes. If your house is older and has original fixtures, ACV might save you some money—though you’ll risk bigger out-of-pocket costs.

Extended/Guaranteed Replacement Value Upgrades

Extended Replacement Cost pays 20-25% above your dwelling coverage limit if rebuilding costs go up after a disaster. Construction prices often spike after storms.

Guaranteed Replacement Cost covers everything it takes to rebuild, regardless of the cost. It’s the priciest option, but it’s the most peace of mind you can get.

Extended coverage typically adds $100-$ 200 per year. Guaranteed replacement can increase your premium by $300-$ 500 annually.

You’ll need to update your home’s value every year to keep your coverage accurate.

Protect your Huntsville home with Woodall & Hoggle Insurance Agency. Compare personalized homeowners insurance options today—get peace of mind and coverage that fits your family. Contact us.

If you’re ready to get

started, call us now!

3- Review Deductibles Carefully

Your deductible affects both your premium and what you pay out-of-pocket if you file a claim. Huntsville homeowners face unique deductible structures, particularly for wind and tornado damage.

Flat vs Percentage Deductibles

Most policies offer flat dollar deductibles. These remain the same regardless of your home’s value.

In Huntsville, flat deductibles usually run from $500 to $2,500. If you pick a $500 deductible, you’ll pay around $2,963 a year; higher deductibles mean lower premiums, but more out-of-pocket if disaster strikes.

Percentage deductibles make you pay a chunk based on your home’s insured value. For example, a 2% deductible on a $300,000 house means you’re out $6,000 before insurance kicks in.

Flat Deductible Benefits:

Easy to predict

Lower out-of-pocket costs for pricier homes

Simpler to budget for emergencies

Percentage Deductible Drawbacks:

Expensive for high-value homes

Harder to predict costs

Could cause financial stress

Tornado/Wind Deductibles Common in North Alabama

Insurers in Alabama often require separate wind and hail deductibles due to the state’s unpredictable weather. These are usually percentages, not flat amounts.

In Huntsville, wind deductibles usually range from 1% to 5% of your dwelling coverage. So if you’ve got a $250,000 home and a 2% wind deductible, you’ll pay $5,000 out-of-pocket for tornado damage.

Most insurers use wind deductibles for both wind and hail claims. That includes damage from thunderstorms, tornadoes, and other severe weather we see up here.

Wind deductible facts:

Applies per claim, not per year

Covers roof, siding, and window damage

Usually can’t be waived or lowered

Separate from your regular deductible

Some policies mention hurricane deductibles, but these are rarely invoked in Huntsville. Still, you might see them in your paperwork.

4- Don’t Skip Flood Insurance

Standard homeowners’ insurance won’t cover flood damage in Huntsville. The National Flood Insurance Program (NFIP) provides federal coverage, while private insurers offer their own options with varying benefits and price points.

NFIP vs Private Flood Insurance

The NFIP gives you government-backed flood coverage with set rates and terms. Their policies cover up to $250,000 for your home and $100,000 for your stuff inside.

Private flood insurers usually offer higher limits than NFIP. They might also cover extra living expenses if you need to relocate during the repairs.

NFIP vs Private Flood Insurance:

Coverage limits: Private insurers often go higher

Cost: Private policies can be cheaper for newer homes in low-risk areas

Claims process: Private insurers tend to process claims faster

Waiting period: Both usually have a 30-day wait before coverage starts

Some flood insurance companies offer replacement cost coverage, but NFIP sticks with actual cash value for older homes. Always shop around—rates can be all over the map.

Local Floodplain Mapping Tools

FEMA flood maps show risk zones across Madison County and Huntsville. These maps help lenders determine if you need flood insurance and assist in setting your premium.

Zone AE indicates a high flood risk and requires mandatory insurance for mortgaged homes. Zone X is considered a lower risk area, but flooding can still occur—especially during major storms.

Huntsville flood risk factors:

Close to the Tennessee River

Spring Hill and Monte Sano drainage

More urban development means more runoff

Heavy rain in certain seasons

You can check flood zones with FEMA’s online tool. Local building departments also keep updated floodplain maps.

Even if you’re not in a high-risk zone, it’s worth considering flood insurance. Approximately 25% of flood claims originate from moderate or low-risk areas, and coverage is typically more affordable in these areas.

Don’t risk uncovered flood damage in Huntsville. Woodall & Hoggle Insurance Agency helps you secure affordable NFIP and private flood policies—schedule your coverage review today.

If you’re ready to get

started, call us now!

5- Ask About Roof and Weather Discounts

Insurance companies in Huntsville give significant discounts if you’ve got wind-resistant roofing or storm protection features. With the right upgrades and paperwork, you could cut your premium by 5-25%.

Proofs Insurers Require for Credits

Insurance companies require specific documents before approving roof or weather discounts. Just telling them you upgraded your roof won’t cut it.

Required Documentation:

Building permits for roof installations

Contractor invoices with material specs

Wind mitigation inspection reports

Photos showing installation details

Manufacturer warranties for impact-resistant materials

Most insurers require a wind mitigation inspection performed by a certified inspector. That’ll run you $75-$ 150, but it can save you hundreds of dollars every year.

The inspector checks a few main things:

Roof covering materials

How the roof deck is attached

Roof-to-wall connections

Wall construction type

Window and door protection

Impact-resistant shingles need to meet Class 3 or Class 4 UL standards. Insurers typically deduct 10-20% for Class 4 shingles.

Storm shutters or impact windows must carry Miami-Dade County approval or an equivalent certification. Insurance companies double-check these through product databases.

Impact of Roof Age on Policy Costs

The age of your roof really affects your insurance premium in Huntsville. Older roofs mean higher rates and, sometimes, less coverage.

Premium increases by roof age:

0-10 years: Standard rates

11-15 years: 10-15% increase

16-20 years: 20-30% increase

20+ years: 40-50% increase or coverage denial

Lots of insurers limit coverage if your roof is over 15 years old. They’ll often only pay actual cash value instead of the full replacement cost on older roofs.

Some companies recommend roof inspections once your roof reaches 10 years. If your roof fails, they might just cancel your policy.

New roof benefits:

Full replacement cost coverage

Lower deductibles available

Access to more discounts

Easier policy renewals

6- Bundle and Secure Your Home

Bundling home and auto insurance, installing monitored alarms, and maintaining a claims-free status can save hundreds of dollars per year in Huntsville.

Huntsville homeowners can save up to 40% just by using these strategies. Not bad, right?

Alarm/Security Savings

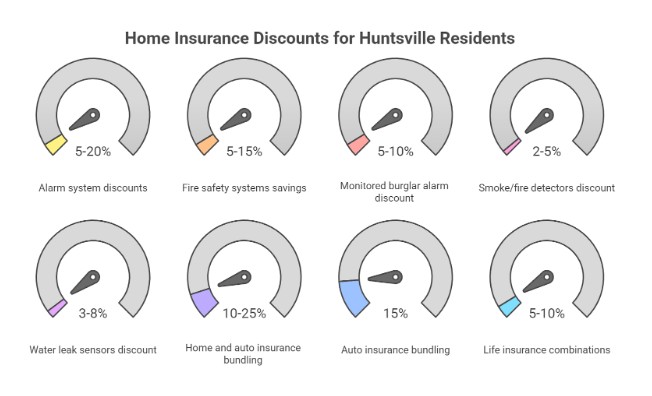

Security system discounts reward you for lowering theft and damage risks. Most Huntsville insurers offer discounts of 5-20% for professionally monitored alarm systems.

Fire safety systems offer the biggest savings. Smoke detectors, fire alarms, and sprinklers can drop your premiums by 5-15%. Water leak detectors and auto shutoff systems also get you discounts.

Burglar alarms must be connected to a central monitoring station to qualify for a discount. Self-monitored setups usually don’t qualify. The monitoring company needs to alert the police or the fire department directly.

Smart home security is finally catching on. Video doorbells, smart locks, and connected cameras are now eligible for new discount programs.

Security Feature

Typical Discount Range

Monitored burglar alarm

5-10%

Fire sprinkler system

5-15%

Smoke/fire detectors

2-5%

Water leak sensors

3-8%

Multi-Policy Savings with Auto or Umbrella Coverage

Insurance companies give their biggest discounts to customers who buy more than one policy. Bundling home and auto insurance usually saves 10-25% on both.

Auto insurance bundling is the most common. Huntsville residents can save approximately 15% by combining home and car coverage with the same insurer.

Umbrella policy additions add extra liability protection and more discounts. Adding $1 million in umbrella coverage often costs under $200 a year and triggers bundle savings.

Life insurance combinations with the same company can unlock additional discounts. Some insurers knock off another 5-10% if you combine three or more policies.

It’s smart to compare bundled prices against separate policies from other companies. Strategic comparison shopping makes sure you’re actually saving money—and not just seeing a lower number on paper.

7- Work with an Independent Insurance Agent

Independent agents can access lots of insurance companies to find coverage that fits your unique risk profile. Local agents in Huntsville truly understand the weather patterns and building codes that matter most for your policy.

How Independent Agents Find Underwriting Fits

Independent agents work with several insurers instead of just one. That lets them check out different underwriting guidelines for each carrier.

Every insurance company has its own preferences. Some like newer homes built after 2000. Others specialize in older houses or homes with claims in the past.

An agent looks at your property details and claim history. Then they match you to the carrier most likely to offer a good rate.

Key factors agents evaluate:

Home age and construction materials

Previous insurance claims

Credit score requirements

Location-specific risks

Say your home has an older roof. The agent knows which companies still offer full coverage and which ones demand an update.

This targeted approach saves you time and usually lands you a better deal than shopping solo.

When Local Agents Beat Direct Writers

Local Huntsville agents are familiar with the regional quirks that online companies often overlook.

They know which carriers handle Alabama weather claims quickly—and which ones drag their feet.

Direct online companies use automated systems. Those can’t always account for local issues. A local agent can explain why certain coverage limits matter more in tornado-prone areas.

Local advantages include:

Knowledge of flood zone changes

Relationships with claims adjusters

Understanding of local building codes

Experience with Alabama-specific coverage needs

Independent agents can also bundle home and auto insurance with the same carrier to receive additional discounts. They handle policy changes and claims support right here, not through a call center.

When you need to file a claim, local agents go to bat for you with the insurance company. That personal touch often speeds things up compared to dealing with some far-off customer service desk.

What Huntsville Clients Say About Woodall & Hoggle Insurance Agency

Honest feedback from Huntsville homeowners and businesses highlights why so many trust Woodall & Hoggle for their insurance needs:

Daniel Gibson shared that during his home purchase, “Elicia was very professional but still remained personable. When I asked questions, she took the time to explain everything clearly.”

Amy Lea noted, “They are always willing and eager to help and easy to get in touch with by phone or email. Elicia Wright has been amazing to work with and always quick to respond. Friendly home town feel!”

Claude Moore praised the agency’s long-term service: “Woodall & Hoggle has been handling our company’s liability insurance for years, and we couldn’t be more pleased. Chris Hoggle and Elicia Wright’s responsiveness and professionalism are always appreciated.”

Miranda Miller said, “I called for a business quote and Elicia answered my dozens of questions without pressure. She gave me the best options, and I’ll be recommending them to all my contacts.”

Final Takeaway

Shopping for homeowners’ insurance in Huntsville? You’ll want to compare several providers and their coverage options.

The city has both national carriers and regional companies that really get Alabama’s unique risks.

It’s smart to collect quotes from at least three different companies. Rates in Huntsville typically start around $298 per month, but they can vary significantly depending on your coverage and the specific details of your home.

Cheapest isn’t always best. Coverage quality, customer service, and how a company handles claims—they’re just as important as the price tag, maybe even more so.

Residents in Huntsville should review their policies every year. Property values shift, and insurance needs change too.

If you work with local insurance agents, you can get insights that national providers might miss.

These individuals are familiar with tornadoes, flooding, and other local hazards that can affect your coverage in north Alabama.

Bundle home and auto insurance with Woodall & Hoggle Insurance Agency to save more each month. Protect your family and property with confidence—contact us to get started.

Contact Us Today For An Appointment

Frequently Asked Questions

What is the average cost of homeowners’ insurance in Alabama?

The average Alabama homeowner pays $3,400–$4,100 per year in 2025, with premiums in Huntsville varying by roof age, claims history, and location within Madison County.

Does homeowners’ insurance cover flood damage in Huntsville?

No. Standard homeowners’ policies typically exclude coverage for flood damage. You’ll need to purchase separate flood insurance through NFIP or a private carrier, even if you live outside FEMA flood zones.

Does homeowners’ insurance cover tornadoes and hail?

Yes, tornado and hail damage are generally covered, but check your wind/hail deductible. Many Alabama policies use percentage-based deductibles, which can significantly affect out-of-pocket costs.

Should I choose replacement cost or actual cash value coverage?

Choose replacement cost whenever possible. It pays the full cost of rebuilding or replacing property without deducting for depreciation, unlike actual cash value policies.

How can I lower my homeowners’ insurance premium in Huntsville?

Bundle home and auto, maintain a claims-free history, install monitored security systems, and update your roof to qualify for discounts and reduce premium costs.

Does roof age impact homeowners’ insurance in Huntsville?

Yes. Older roofs often trigger higher premiums or actual cash value settlements. Newer or fortified roofs may qualify for substantial discounts.

Do lenders require homeowners’ insurance in Alabama?

Yes. Mortgage lenders require dwelling coverage at least equal to your loan amount, but choosing higher limits can better protect against Huntsville’s rebuild costs.

Why work with an independent insurance agent in Huntsville?

Independent agents represent multiple carriers, helping you compare options, secure discounts, and tailor coverage to North Alabama’s weather and rebuild risks.